Life, Liberty, Property #134: Make Housing Affordable Again: Unlock the Supply Side

Published February 17, 2026

Life, Liberty, Property #134: Make Housing Affordable Again: Unlock the Supply Side

Forwardthis issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

Make Housing Affordable Again: Unlock the Supply Side

Video of the Week: The Next Big Crash — In the Tank Podcast #526

This edition of Life, Liberty, Property presents a single essay on a complex subject: the housing affordability problem and President Trump’s proposals to deal with it. A free-market perspective on affordability requires attention to the myriad ways in which government has undermined markets.—STK

Make Housing Affordable Again: Unlock the Supply Side

Young New Yorkers are gorging on fancy food while complaining that they cannot afford to buy houses, a Wall Street Journal article on luxury grocery stores in Manhattan stated last week:

Gen Zers and millennials are swimming in student debt and may never own homes, but they’re splurging on gut-healthy juices and rotisserie chickens. New York City as a whole is in the midst of an affordability crisis, one that helped elect Mayor Zohran Mamdani, yet a new crop of luxury prepared-food purveyors is drawing massive crowds in Manhattan and driving social-media discourse. Influencers fill aisles in search of trendy nut butters and overpriced salads. The stores are packed on weekends with teens who inhale frozen yogurt.

Understandably, the comment drew heavy fire on the internet after the Journal inexplicably posted a quote on X:

Many commenters noted that a rotisserie chicken costs $4.99 at Costco. The median purchase price for a home in the United States was $396,800 in January, and more than 75 percent of U.S. homes on the market are unaffordable for those earning the median wage. Home affordability in the United States is well below the historical average, and the problem has increased in recent years, Realtor.com reported last month: “Since 2020, home prices have risen 54%, far outpacing the 29% gain in typical wages, according to ATTOM’s analysis of Labor Department data.”

Young people’s difficulty in affording houses is neither their fault nor a mirage. “The typical household earns almost $80,000 a year, according to the Claritas estimates of U.S. Census Bureau data, far less than the $113,000 needed to afford a median-priced home of $435,000 as of July,” Bankrate reports. “A prospective homebuyer’s income would need to top $200,000 to afford the median-priced home in Seattle, San Francisco and New York, according to Bankrate’s analysis.”

It would take a median-income family seven years to save up the down payment for a house at the U.S. household’s average annual saving rate of 5.1 percent, the Unleash Prosperity Hotline reports. In the San Francisco metropolitan area, it would take 36 years. (Boy!) The same is true of San Jose, and it would take 34 years in Los Angeles, 30 in San Diego, and 23 in Boston, Seattle, or New York.

Obviously, that is not a sane situation.

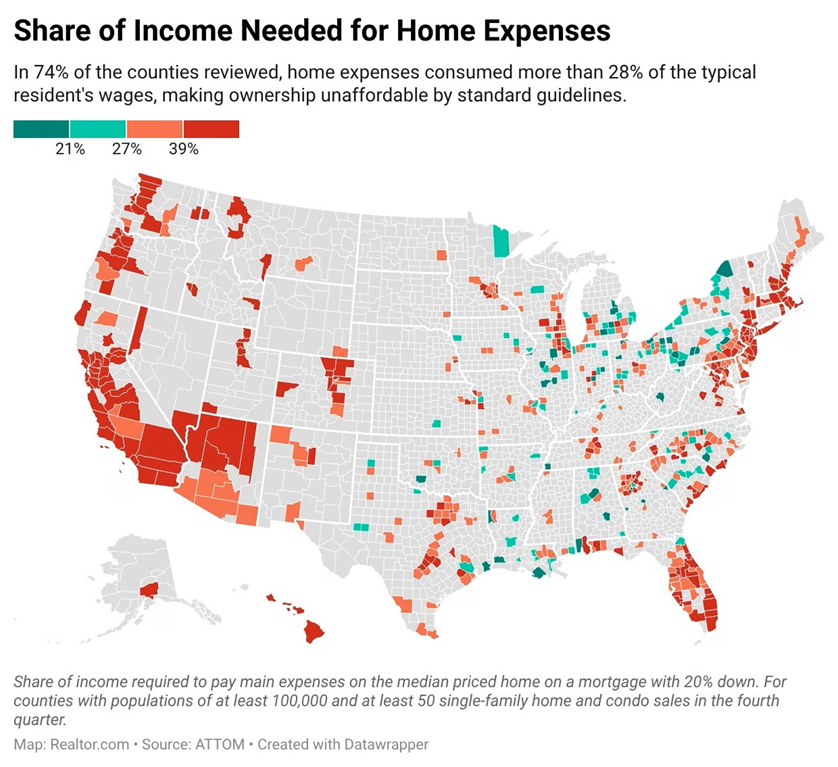

Seven of the ten cities with the least affordable housing in the world are in the United States, Realtor.com reported last week, and home ownership is unaffordable by historical standards in 74 percent of counties reviewed by Realtor.com for the site’s January report:

As the data above show, the powerful inflation surge of 2021 through mid-2023 hit the housing market especially hard, and high interest rates imposed by the Federal Reserve to counter the monetary expansion made the cost of buying a house even more daunting. Housing prices have yet to moderate by much, though they are showing signs of a slow contraction, with just under one-fifth of the listings for new homes in the fourth quarter of 2025 showing price cuts and 18 percent of existing homes listing decreases.

Presidential Premises

People understandably look to the president for leadership in a crisis, real or perceived. President Donald Trump has obliged with a flurry of proposals. Unfortunately, although some of the ideas Trump has offered are quite good, others would cause more government interference in the housing market and would not benefit those who wish to buy or sell a house.

Trump’s proposals have always reflected the improvisational nature typical of his public pronouncements on policy issues. What is very good about that is his willingness to reverse course once convinced that an idea is off base. His major current premise on housing is very much so.

Trump revealed a central premise behind his various proposals when he stated at a January 29 Cabinet meeting, “I don’t want to drive housing prices down. I want to drive housing prices up for people that own their homes, and they can be assured that’s what’s going to happen.”

The promise that homeowners would not face a loss of value in their houses, which for millions of people provide the largest share of their personal wealth, fully contradicted the president’s pledge to make housing more affordable: “We’re not going to destroy the value of their homes so that somebody who didn’t work very hard can buy a home,” Trump said.

Prices and Values

That may be good politics, but it is bad economics. Writing at his Regime Critic website, economic policy analyst and Ph.D. student Josiah Lippincott points out that lower prices of housing would be good for everybody, even those who own their homes outright:

Falling prices are good for people with monthly payments. Downward pressure on housing means that current owners when they move can get a better deal. Let’s look at the example of someone who owns their home outright. Let’s say there is a large expansion in housing construction and the price of his home falls in half. This does not harm him. Why?

First, even if he sells his home for half what he paid for it, the price of housing more broadly has fallen in half. When he goes to buy a new home that home is also half as expensive as it would have been.

The owner has not lost money. He has not lost out on opportunities to buy new housing just because their price has fallen.

Similar factors apply to those who are currently paying mortgages on expensive houses and want to move, and even for those who are underwater on their mortgages, owing more than their house is worth even at the elevated prices of recent years, Lippincott writes: “The homeowner loses nothing if he doesn’t sell. He can keep paying on his current mortgage as long as he has a job. The longer he keeps paying, the closer he gets to breaking even on the house.”

From a simple numerical perspective, the idea of growing one’s wealth through home price appreciation is absurd. To access such increases, one must sell the home and simultaneously buy another. But, all else equal, the price of the home being acquired has also gone up to the same degree, so there is no net benefit. There is in fact a net negative in the form of transaction costs—commissions, moving, and other related expenses.

Taking home equity loans is even worse. Accessing liquidity from home equity in this manner does absolutely nothing to increase homeownership wealth. Once the home equity facility is drawn, the owner becomes a borrower. Any cash he has borrowed is offset by the corresponding loan liability. That loan immediately begins accruing interest—usually at a high rate—further undercutting any supposed financial benefit.

There is one notable instance where home equity can be used to achieve financial ends deemed desirable by the owner. That is a downsizing of the variety undertaken by seniors, often shortly after their children have grown up and moved out. And therein lies the rub. When housing is viewed as an investment by a cohort of politically-vociferous Americans, a policy of monetary debasement and asset inflation by the administration will follow in order to appease that cohort. The president admitted as much in the White House.

None of this makes housing more affordable, but it explains why politicians are exceedingly reluctant to make housing more affordable in real-dollar terms instead of using inflation to confuse everyone into thinking that houses are not wildly overvalued and due for a “correction” of very significant and wrenching proportions.

Lippincott’s argument relies rightly on a recognition that there is only one thing that will make housing prices fall in real, inflation-adjusted terms: an increase in supply. Trump’s idea, Lippincott argues, is to keep current homeowners happy with the rising dollar-denominated value of their homes while increasing the ability of people to buy those homes, by pushing interest rates down.

That is simply a recipe for more inflation, Lippincott observes; and inflation, government-induced, is precisely what got us into this affordability problem in the first place, as I have argued in previous issues of this newsletter. The real solution to the housing affordability problem is to build more houses. That is the only way to decrease the real price of housing: more supply.

Boomer Housing Trap

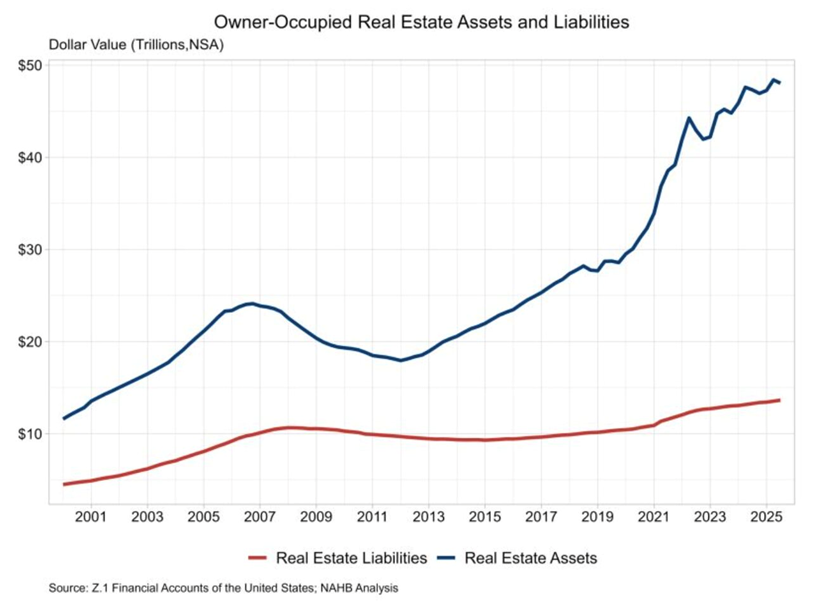

The rapid and unwarranted rise in nominal housing values is preventing homes from going on the market. The baby boomers and empty nesters are sitting on $50 trillion in owner-occupied housing, four times what it was worth in 2020, the Hotline reports:

Even better news: The owner equity share of that $50 trillion has steadily risen to 72% (up from 48% just 10 years ago). The remaining 28% is owned by lenders and investors. This means that Americans directly own nearly $35 trillion of the housing stock. We are a VERY rich nation.

That is a great thing for the boomers. It is, however, a big burden on the rest of the nation’s population. In a true market system, boomers would be selling their houses and moving into smaller ones, thereby contributing to the social good of giving larger families bigger homes. Persistent inflation has discouraged that by causing people to view their homes as hard assets that provide more-reliable value than a falling dollar. That has driven housing prices up and intensified the hedge effect.

A major additional factor is a government policy, naturally: capital gains taxes. Here’s how the Hotline describes the situation:

The big housing mystery is why aging baby boomers and empty nesters haven’t cashed in on that equity and sold their homes to the younger generation—effectively, their children.

Answer: because they can’t afford to sell because the capital gains tax owed would be so high. They are locked in. Instead, the boomers sit on the homes like a mother hen and wait until they die to avoid paying the tax.

Monetary inflation is the primary cause of those rises in prospective capital gains taxes. The government exempts the first $250,000 of capital gain from taxation, and $500,000 for couples filing jointly. That number has not been adjusted for inflation since 1997. Prices have more than doubled in the United States since then, and housing prices have nearly tripled.

The government punishes people for a nominal appreciation in the values of their houses, which is not real. Little wonder that baby boomers are staying barricaded in their homes. This tax brutality is distorting the housing market radically, keeping one- or two-person households in big houses and jamming families with children into smaller ones. It is absolutely stupid and cruel.

Rep. Craig Goldman (R-TX) has introduced a bill to cut that tax. Goldman’s Don’t Tax the American Dream Act would eliminate capital gains taxes on sales of primary residences for homeowners who have lived at the property for at least two years.

That would be a highly beneficial reform. Instead of ordering people about, Goldman’s bill would remove a government impediment to millions of potentially mutually beneficial transactions. Trump suggested this last July, and he is right to support the idea.

A Flurry of Conflicting Policy Proposals

Unfortunately, President Trump is pushing several ideas that would expand demand further while doing little to increase supply. Trump proposes to have Fannie Mae and Freddie Mac buy $200 billion of mortgage-backed-securities, allow people to use money in their retirement accounts to cover down payments for houses, require lenders to allow borrowers to shift their mortgages to different homes (“portability”), and allow 50-year mortgages (which Trump has since withdrawn).

Trump’s executive order to discourage large investors from buying single-family homes is likewise misdirected. Reducing the number of potential buyers for houses will lower prices (reduced demand means lower prices for the same supply), which is an unjustifiable interference and works against the president’s (ill-advised) goal of keeping housing prices high. It would also suppress supply by decreasing investment in rental homes. That is the opposite of what needs to happen.

Trump’s executive order is not as intrusive as one might think, as I wrote in Life, Liberty, Property number 131, though it is misguided in reducing the supply of investors in single-family homes. The best element of the president’s proposal is the exemption that allows these companies to build rental homes. TheNew York Times characterizes this provision as a terrible loophole that ruins the plan, though that idea seems to have been imposed by the editors on a story that reports the facts rather fairly otherwise:

The build-to-rent exemption may seem at odds with the Trump administration’s stated goal of making more homes available for sale to middle-income Americans by cracking down on Wall Street-backed landlords. Similar proposals have garnered support from some Democratic and Republican politicians over the years.

But housing analysts say, from a policy perspective, build-to-rent communities make sense because they are improving the availability of quality rental housing.

Rick Palacios Jr., director of research for John Burns Research and Consulting, a housing research firm, said build-to-rent communities catered to parents with young children who weren’t quite ready to buy a home.

“Build-to-rent is really a natural steppingstone for homeownership,” he said.

That provision is a good supply-side measure, though it should not be necessary. Investors with more than 1,000 properties own just 2 percent of small-unit rental properties. Encouraging investors to increase that number by building new homes would be a positive step.

Expanding the Housing Supply

Trump should drop those conflicting and contradictory proposals and concentrate on the important side of the price equation: supply.

The president’s call for states and localities to cut zoning and other regulations that make housing more expensive to build would make a huge difference—if those governments do as he asks. Trump and the Congress should make sure that the states and localities do that, by making it a requirement for receipt of federal housing subsidies and funding for transportation and other infrastructure projects (none of which should exist anyway).

The leaders of the (admittedly narrow) Republican majorities in Congress should put that in the next reconciliation bill, which would avoid a Senate filibuster. If there are complexities involved, they should figure out the solutions and get it done.

Another excellent supply-side idea is the proposal for “Trump homes.” Major homebuilders are discussing a cooperative, private-sector plan to build up to a million entry-level houses for first-time buyers across the country, as President Trump called upon them to do last fall.

The building project would be funded by private investors and directed toward first-time buyers. The New York Post reports:

The homes would be intended to provide a pathway to homeownership for first-time buyers, with one version of the plan allowing for monthly rental payments over three years to be applied toward a down payment, in a version of rent-to-own, the sources said.

The plan may need some federal deregulation, the Post notes: “Although the plan would be privately funded, to be profitable for the builders, it might require changes to the mortgage guarantees offered by federally controlled mortgage giants Fannie Mae and Freddie Mac.”

Since last fall, unfortunately, Trump has backed away from the idea, in favor of keeping house prices high. “In other words, you create a lot of housing all of a sudden, and it drives the housing prices down,” Trump said at his January 29 Cabinet meeting.

The president should renew his support for building Trump homes and offer the boomers a big compensatory bounty in the elimination of the capital gains tax on sales of primary housing. Allowing prices to fall to match their real values to people is always a good thing.

There’s a lot to like about the idea. Renting first to make sure buyers have the financial wherewithal to become owners makes sense. The concept is far better than the costly subsidized rentals that Democrats favor—through the low-income housing tax credit or, even worse, a new era of public housing. But Trump Houses will only work if they truly meet the criteria for starter homes—small houses on small lots that are naturally affordable as a result.

Those houses would fill an important gap in the market, Husock notes:

Starter homes have become scarce in America. Small houses on small lots were once common—for example the 1146 square foot home in Dalton, Illinois purchased new in 1949 by the parents of the boy who became Pope Leo. The median new house today is more than 2100 square feet. The typical house lot is more than 9,000 square feet, compared to the 4900 square foot size of the Pope’s family’s.

A million Trump houses could enable young people to get an affordable start on the American Dream, as the equity they accumulate would qualify them to buy bigger houses as their families grow. Deregulation of state and local impediments to housing will be crucial, however. Husock writes,

[B]uilders will only be able to build Trump Houses if local communities will let them do so. There are more than 30,000 “zoning jurisdictions” in the US—that is, municipalities and other government entities that decide the size of homes and their lots than are permitted in their communities. They are the front lines of “Not in My Backyard” decisions that zone out new home building. Among the most exclusionary are found in blue states that may not take to the Trump brand.

Husock says Trump or Housing and Urban Development Secretary Scott Turner will have to “use their bully pulpits to convince communities that Trump Houses are a good idea.” That will not happen. Instead, the president and Congress should use federal-funding reductions to punish states that do not liberalize their laws, as I noted above.

Trump has already done many of the most important things needed to solve the affordability problem, including the housing element: stopping inflation, lowering interest rates, cutting energy prices, eliminating unnecessary regulations, and reducing taxes. Those are all actions that ease government’s suppression of the production of goods and services.

Not all of the effects will not be apparent immediately. In the long term, however, these reforms will prove immensely beneficial.

Trump and the Congress should build on those ideas and scuttle all of those that conflict with the aim of lowering housing prices in real-dollar terms. They should recalibrate toward policies that increase the supply of housing. That largely means removing the impediments that have been erected by the federal, state, and local governments.

That is the real and long-lasting solution to the affordability problem. There is no other.

Justin Haskins joins us to talk about his and Jack McPherrin’s new book, “The Next Big Crash,” covering the shady dealings of Wall Street insiders and elites who have conspired to rig our economy and transfer control over our futures to massive financial interests. When the next crash comes, it could very well be more devastating than any before.

On a brighter note, federal employment is at the lowest level it has been since 1966, showing that the Trump administration really has made progress on cutting federal bloat, while American private sector jobs are improving. Meanwhile, the SAVE America Act may be passed soon, but Democrats say it will disenfranchise voters by requiring them to simply have ID.

On UNHINGED: How would you feel about living in a constant, ubiquitous surveillance state? Ring is more than happy to provide, but promises it will only be used for finding lost dogs.

The Heartland Institute’s Linnea Lueken, S. T. Karnick, Jim Lakely, Chris Talgo, and guest Justin Haskins will talk about all of this and more on Episode #526 of the In The Tank Podcast.

Important Heartland Policy Study

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org

{kind=link}