Life, Liberty, Property #146: Are Markets Calling for an Interest Rate Hike?

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

Are Markets Calling for an Interest Rate Hike?

Video of the Week: The Cost of Living Crisis — In the Tank Podcast #537

How to End Quantitative Easing Without Destroying the Economy

Breaking the Power of Teachers Unions

Hot off the Presses!

‘Today’s crisis is a product of government errors, not greedy landlords, institutional investors, and so-called market failure.’

Are Markets Calling for an Interest Rate Hike?

As Kevin Warsh takes over as chairman of the Federal Reserve (Fed), investors and analysts are expressing much worry about interest rates. The argument is that the Fed may be forced to raise interest rates in direct contradiction to President Trump’s stated preference for a rate cut, as oil price increases threaten to push up prices everywhere and spur a return toward Biden-era inflation rates.

The bond markets, the story goes, are signaling expectations of an interest rate increase to fight inflation, The Wall Street Journal reports:

Investors are giving up on Fed rate cuts and pushing up bond yields. That in turn makes borrowing more expensive.

Some economists now argue the Fed will have to seriously consider raising rates, not just keeping them where they are. If the Fed holds steady but inflation keeps rising, that means the Fed has effectively adopted looser monetary policy just by standing pat.

This crisis is in the Treasury market. Bond yields are moving sharply higher, and they are sending a message that policymakers can no longer afford to ignore: the financial system is becoming unstable under the weight of war spending, massive deficits, persistent inflation, and a debt load that was already unsustainable before this conflict began. …

The 10-year Treasury yield is arguably the single most important price in global finance because virtually every major asset class is built on top of it. Mortgage rates, commercial real estate valuations, private equity models, corporate borrowing costs, equity multiples, venture capital, and government financing itself all depend on stable Treasury markets. When yields rise too quickly, everything starts repricing at once. That is why this matters so much more than the daily moves in the stock market.

Last Friday [May 15] closed with the 10-year Treasury yield at 4.60%, a one-year high, and the doom commentary about rising interest rates was waiting before the bell even rang. Hyperinflation. Bond market breakdown. Paradigm shift. A 1981 fair-value retest. The Fed is about to “push the brrrr button” or pop “the everything bubble.” If you spent any time on social media over the weekend that followed, you saw a version of every one of those.

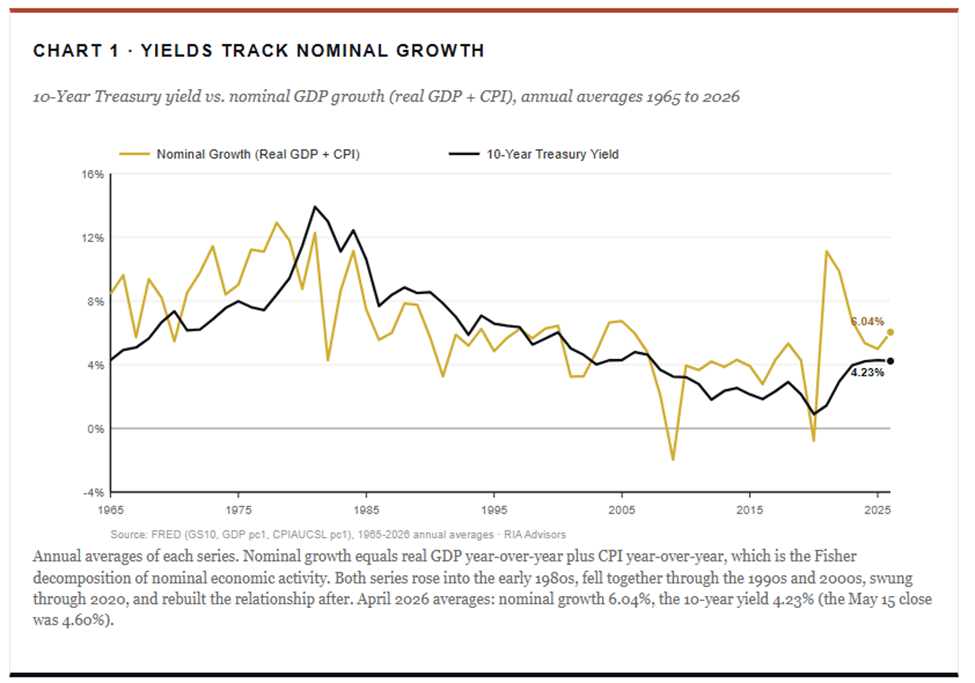

So I posted a short thread that Friday, making a simple point. Over time, yields track growth and inflation. The chart that drew the strongest pushback roughly showed that relationship, and a wave of responses argued that the framework is broken, debt is about to break the bond market, supply-side inflation has changed everything, and rates have nowhere to go but higher.

The data show that current Treasury bond yields are tracking normally with nominal growth of gross domestic product, Roberts writes:

Start with the basic identity behind rising interest rates. Of course, a bond yield is what an investor demands to hold a piece of paper for ten years. That demand has two main inputs: the opportunity cost of economic growth and the inflation rate that erodes the dollars being repaid. If real growth is 2.5% and inflation is 3.5%, then a 6% nominal yield breaks even before any term premium.The investor isn’t going to lend at 2% in a 6% nominal economy because that’s a guaranteed loss of purchasing power and a worse return than the broader economy offers. …

… However, the relationship deserves a more precise statement than “yields track nominal growth.”Over the full 1953 to 2026 monthly history, the 10-year yield has averaged about 0.77 percentage points below nominal growth. Not above, below. So the right way to think about the framework is that yields run slightly below the nominal economy in a stable long-run relationship, and the gap between them has fluctuated within a band rather than collapsing or exploding.

Where does that put us now? Real GDP grew at an annualized rate of 2.0% in Q1 2026. Headline CPI ran 3.8% year over year in April.Together, that puts nominal growth on a 6.04% pace. The 10-year at 4.60% sits about 1.7 percentage points belownominal growth, a gap roughly a full point wider than the long-run average. By the mean-reversion logic the framework implies, the fair value of the 10-year is closer to 5.3% than to 4.6%.

Therefore, yes, there is modest upward pressure on rates from here. However, that is a very different statement than “7% rates and a debt crisis.” It is a slow drift back toward a long-established relationship, not a paradigm shift.

Expectations about inflation are critical to bond prices and yields (which move in opposite directions), but it is important to keep in mind that the investors’ decisions are based on long-term expectations, not temporary disruptions, Roberts writes:

If a bond pays a fixed nominal coupon and inflation runs at 4% over the life of that bond, every dollar the investor receives back is worth less than the dollar they originally lent. Therefore, bond buyers demand compensation for inflation on a point-for-point basis. If they expect inflation to average 3% over the next ten years, they want at least three percentage points added to whatever real return they require. If they expect 5%, they want five points. The framework is built on the assumption that bond buyers are not in the business of giving away purchasing power.

The word expected matters more than most casual observers appreciate. The Fisher equation is not about what inflation prints today. It is about what investors expect inflation to be over the bond’s remaining life. If headline CPI runs 4% in April but the bond market believes inflation will average 2.5% over the next decade, the 10-year yield will reflect that 2.5%, not today’s 4%. This is exactly why short-term inflation spikes do not always translate one-for-one into yield spikes. Markets are pricing the forward path, not the rearview mirror. So when commentary points to a hot monthly print and asks why yields are not breaking out, the Fisher framework is the answer.

Given that 10-year bond prices are all about long-term inflation expectations, the current price makes sense, is within historical norms, and does not indicate a crisis in the financial system, Roberts notes:

A regime shift in nominal yields, the kind the doom case is forecasting, would require a regime shift in inflation expectations. Not a one-year inflation spike. Not a quarter of hot prints. A permanent re-anchoring of what bond markets expect inflation to average over the next decade. That has happened exactly once in U.S. modern history, between 1968 and 1980, and it took twelve years of policy mistakes, oil shocks, and lost central bank credibility to produce it. The current setup, however uncomfortable, is not that.

Pull this together and apply it to the present moment.

Real growth potential, by every credible estimate, including those of the Congressional Budget Office and the Federal Reserve staff, isaround 1.8% to 2.0%.

Long-run inflation expectations, as measured by the five-year forward breakeven and survey-based measures, are anchored near 2.4%.

Add those two and the framework points to a steady-state 10-year yield in the neighborhood of 4.0% to 4.5%, plus a small term premium.

Today’s 10-year at 4.60% is right inside that range. Slightly elevated, perhaps, but not screaming regime shift.

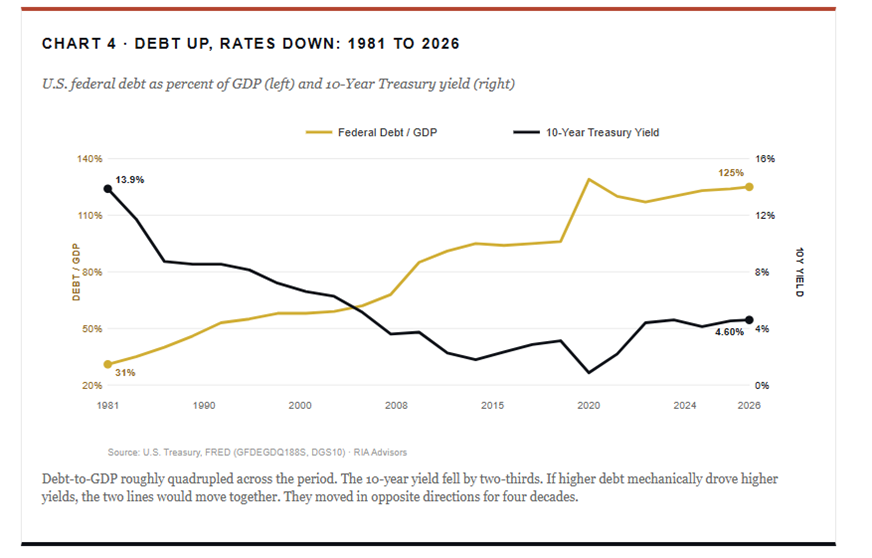

The federal government’s precarious, high-deficit fiscal position is doing serious damage to the economy, Roberts acknowledges. Its effects, however, are not what we are seeing in the Treasury bond price, Roberts writes:

Here is U.S. federal debt as a share of GDP, plotted against the 10-year yield, since the start of the modern era.

… [T]he simple “more debt equals higher rates” thesis fails the empirical test over any meaningful horizon. The reason is that the inflation-and-growth channel runs the other direction. Rising debt service crowds out productive investment, suppresses the marginal return on capital, and slows trend growth. In turn, lower trend growth means lower inflation, which means lower yields. The whole thing self-corrects, just not in the way the doom narrative wants.

If that is all correct, raising interest rates and forcing Treasury bond yields down will only do further harm, and probably a lot of it. What will determine the course of the economy for at least the rest of the year, then, is whether Warsh agrees with Roberts’s analysis and can convince the Fed’s Open Market Committee of it.

Roberts provides a detailed explanation of the important factors and how they affect one another. The article is well worth reading in full.

Gen Z is increasingly despondent that they will never own their own homes, and are extremely negative about the economy. How right are they, and where are they wrong? And what can the Trump admin do about it, if anything?

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

How to End Quantitative Easing Without Destroying the Economy

New Federal Reserve Chair Kevin Warsh has long advocated the central bank reduce its holdings of Treasurys and mortgage-backed securities, to reverse its two-decade policy of quantitative easing. Since the end of the Great Recession in June 2009, the Fed has increased its asset holdings from $606 billion to the current $4.4 trillion, after reaching a record high of $5.77 trillion in June 2022.

The quantitative easing era resulted in easy money at low interest rates. Among the many effects that had on the nation’s economy, the easy money made federal borrowing less expensive (by lowering interest rates to nearly zero) and introduced huge distortions into the economy. The latter include severe asset bubbles which caused massive misallocations of investment and resources and have yet to burst.

The problem is that quantitative easing created a new “normal” in which everyone expects easy money, and the current economy is based on that assumption. Reversing policy on asset purchases could bring on a severe recession by radically reducing the money supply and raising interest rates.

President Trump has said that the Fed should lower interest rates to allow the economy to grow more rapidly. Warsh told the president he agrees.

Writing at The Wall Street Journal, TrendMacro Chief Investment Officer Donald L. Luskin explains how Warsh could break through that impasse: implement a new “Fed-Treasury accord” in which the Fed would transfer a large proportion of the central bank’s assets and liabilities to the U.S. Treasury.

Here is the goal, as Luskin puts it:

It’s a reasonable goal to reduce the central bank’s securities holdings to $2.5 trillion, which is the level of currency in circulation. Until the Fed’s asset-purchasing spree began in the banking crisis of 2008, the level of currency in circulation—determined by market demand, not the Fed—was always approximately the ceiling for the Fed’s asset purchases. Above that, it’s monetization of debt, and that is what Mr. Warsh wants to counter. The pandemic crisis compounded the problem.

In rough terms for illustration, to get to $2.5 trillion, the Fed would have to shed about $3.9 trillion of its assets—$1.9 trillion in Treasury securities and $2 trillion in mortgage-backed securities.

It would also have to shed $3.9 trillion in liabilities, which funded the asset purchases in the first place. About $3 trillion of the liabilities are so-called excess reserves of banks. This is an Orwellian misnomer, because there are no reserve requirements for banks whatever. The $3 trillion is nothing more than deposits made by banks with the Fed—a full-faith-and-credit savings account with daily liquidity, earning a floating interest rate pegged to the policy target.

The other $0.9 trillion is the Treasury’s General Account, where the Treasury parks cash awaiting disbursement—an entangling service the Fed only began providing in 2008.

And here is how to do that without affecting the markets, Luskin writes:

From the Fed’s standpoint, the Treasury would effectively buy back $4 trillion of Treasury and mortgage-backed securities—much as the Treasury does from time to time with outstanding bonds that have become illiquid. That transaction would change nothing for markets. Those securities aren’t in the markets now (they are held at the Fed), and they won’t be in the markets when they are returned to the Treasury.

The Treasury would pay for those securities by assuming $3.9 trillion of the Fed’s liabilities: the $3 trillion of so-called excess reserves and its own $0.9 trillion General Account.

The Treasury would put those liabilities into a new kind of security it has never offered before—what amounts to a savings account. Nothing would change for the banks now holding so-called excess reserves at the Fed. The Treasury savings account would offer full-faith-and-credit, daily liquidity and a floating rate indexed to the Fed’s policy target.

There are additional details that would have to be worked out, Luskin acknowledges. They are, however, surmountable, and this would be well worth the effort.

I have long called for the Fed to reduce its security holdings and cut interest rates a bit. Luskin’s plan would accomplish that, without damaging the economy with an intense quantitative tightening. Luskin writes,

When it’s done, banks would have everything they have today—what the Fed calls “ample reserves”—but they would be parked at the Treasury. The Fed would still be there for all its traditional functions. The federal government overall—considering the Fed and the Treasury together—would have exactly the same assets and liabilities with the same overall risk profiles.

But the distribution of assets and liabilities and of decision-making responsibilities would be optimized. The Fed would go back to being a central bank, and the Treasury to being a treasury.

Luskin’s plan deserves serious consideration. In the decades since President Richard Nixon detached the dollar from gold, Fed policy has reached the point where a doctor asked by a patient whether the medicine will help says, “Well, it couldn’t hurt.”

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Breaking the Power of Teachers Unions

Teachers unions comprise one of the most powerful political forces in the nation—perhaps the most potent of all. The two national teachers unions have close to five million members: the National Education Association and the American Federation of Teachers. State-level unions collect additional dues money from teachers.

National teachers unions spent more than $32 million on political contributions in 2024, with more than 94 percent of it going to Democrats or progressive-left political advocacy groups. State-level teachers unions spent several million more.

The main goal of teachers unions is political and economic power, not the welfare of the nation’s children. In a moment of strange frankness, former American Federation of Teachers union president Albert Shanker allegedly said, “When school children start paying union dues, that’s when I’ll start representing the interests of school children.” That is in fact a rational position, though obviously not a particularly honorable one.

Essayist, comedian, and former political activist Stephen Kruiser makes this point very well in an article published last week at PJ Media. “Unfortunately, a lot of Americans still fall for the Democrats’ for the children spiel, and truly believe that public education is all about teaching the little ones reading, writing, and arithmetic (remember that word?),” Kruiser writes.

On the contrary, Kruiser writes, the ‘“for the children’ spiel” is a smokescreen deployed to hide a relentless pursuit of power:

When we think of union involvement in leftist politics, it is usually the Service Employees International Union (SEIU) that comes to mind first. That’s because the SEIU people tend to be the most visible. They’re actively involved in organizing most lefty protests and responsible for doling out the freebies that they have to offer to get people to them. While the teachers’ unions can be vocal—AFT head Randi Weingarten hasn’t shut her gaping maw since 2008—their leaders tend to hang in the background, writing checks and issuing marching orders to the Democratic National Committee.

Something that doesn’t get talked about often enough is the sheer scale of this grift. The National Education Association isn’t just big, it is the largest labor union in the United States. The NEA has a million more members than second place SEIU. That’s a lot of forced political contributions disguised as member dues. AFT has almost two million members to throw on top of the NEA’s over three million.

Unless there is a miracle and public sector unions are one day outlawed in this country, the best way to weaken the teachers’ unions is through more school choice. That’s why they’re so bitterly opposed to it. Anything that chokes off the lobbying income cannot be tolerated, even if it is what’s best for the children.

For decades, public-employee unions forced government workers to join their ranks and pay their dues to the union leaders, with the government conveniently collecting those fees for them. Political power made that possible, and the forced dues payments generated the political power that establishes and maintains those policies: the unions spend twice as much on political campaign contributions as on representing their members in collective bargaining.

Although the U.S. Supreme Court has ruled that unions cannot require nonmember government employees to pay dues (Janus v. American Federation of State, County, and Municipal Employees, 2018), the states and the unions do their very best (meaning: worst) to keep that a secret and make it exceedingly difficult for workers to opt out. The unions and their legislative minions do all that they can to defy the clear intent of the Court’s directive.

Given these considerations, school choice is a very good and necessary policy at this point, as it provides parents and children with an alternative to union-run schools. That is why the unions fight so hard to prevent it. Choice is a good response to the power of the teachers unions and the ongoing deterioration of government schools.

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org