Life, Liberty, Property #111: Interest Rates Are Too High

Forwardthis issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

IN THIS ISSUE:

Interest Rates Are Too High

Video of the Week: Obama’s Russia-Gate EXPOSED + Hunter’s PR Tour Disaster | In The Tank Podcast #504

Socialism on the Rise in Northern Cities

Cartoon

Bonus Video of the Week: Climate Realism Violates International Law? – The Climate Realism Show #166

Interest Rates Are Too High

Interest rates are too high as the Federal Reserve stubbornly tries to keep the economy from “overheating”–meaning, growing healthily.

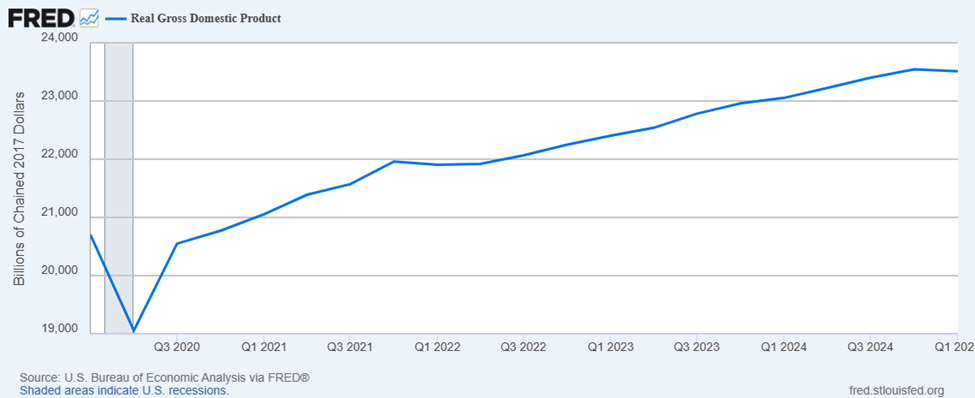

The U.S. economy appears to have begun a recovery this year toward more-natural and productive conditions after years of near-zero interest rates imposed by the nation’s central bank, the Federal Reserve (Fed).

The economic growth rate increased by a full percentage point in the past quarter, The Epoch Timesreports:

The U.S. economy accelerated in July at its fastest pace so far in 2025, according to a closely watched purchasing managers’ survey released on July 24, which showed surging demand for services—even as factory activity slipped back into contraction. …

Overall, the PMI data suggest that the U.S. economy grew at a sharply faster rate at the start of the third quarter—consistent with a 2.3 percent annualized pace of growth—compared with the 1.3 percent that earlier S&P Global PMI surveys signaled for the second quarter, Williamson said.

Growth was uneven, with services strong and manufacturing falling slightly below normal, the paper reports:

The services sector led the gains, with its business activity index jumping to 55.2, hitting a seven-month high.

Factory activity faltered, however, with the manufacturing PMI dropping to 49.5 in July. This was the first reading below 50 this year, indicating a renewed downturn for the manufacturing sector, which President Donald Trump has been trying to revitalize with tariffs and other policies meant to rebuild the nation’s eroded industrial base.

“Real Wages Are Finally Rising Again,” as the Unleash ProsperityHotline reports:

The Bureau of Labor Statistics just released the latest data on median weekly earnings, showing that real weekly earnings are finally back to where they were during the last full quarter of Trump’s first term.

Fortunately, inflation has slowed this year while earnings growth has not. With the passage of the Trump tax bill and other pro-growth measures, we’re expecting that real earnings will continue to rise.

If Kamala had won instead of Trump, the four “lost years” of Biden could’ve easily turned into a “lost decade” like the 1970s.

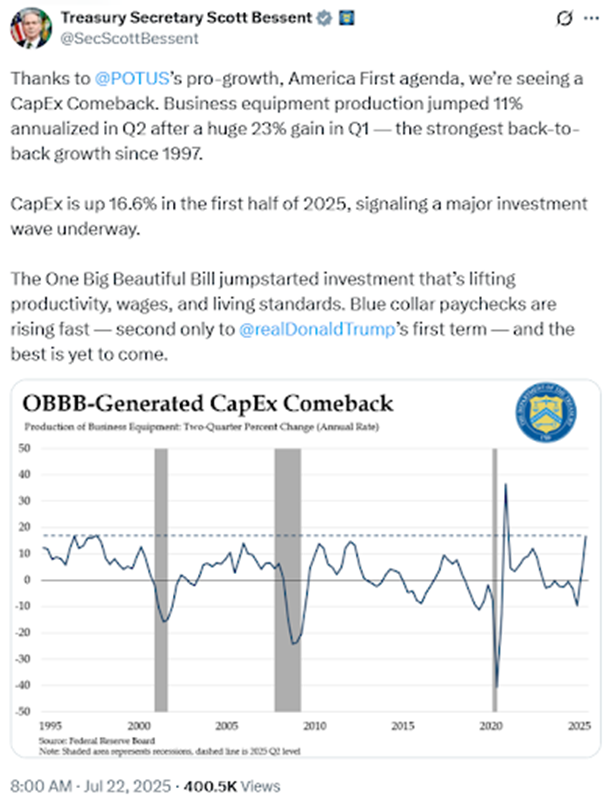

As Treasury Secretary Scott Bessent points out, the Big Beauty’s tax provisions—including 100% capital expensing retroactive to January 19—along with the Trump deregulatory agenda have unleashed a boom in capital expenditures:

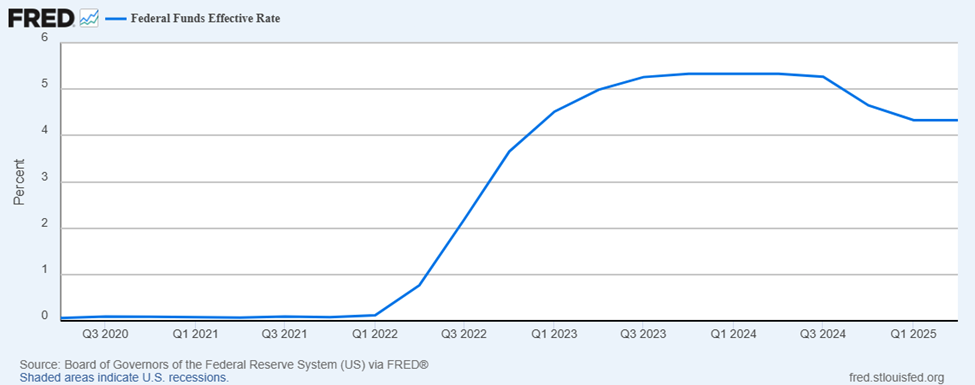

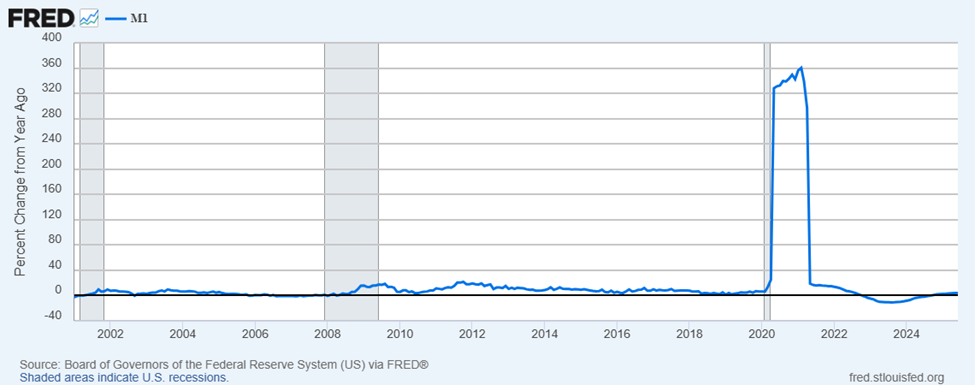

The economic improvement happened in spite of the Fed’s continuation of its post-2021 regime of much-higher interest rates and asset sales slowing and temporarily reversing money-supply growth:

Low interest rates are generally seen as beneficial to economic growth but potentially fueling inflation. Raising interest rates does the opposite, the story goes. The thinking is that cheaper access to borrowed dollars encourages business investment and consumer spending, whereas tighter money makes investment and consumer spending more expensive, and that the consumer and producer spending trends reinforce one another.

Cheap money, however, can cause misallocation of resources as businesses pursue less-productive activities. Cheap money also discourages personal savings (exacerbated in this century by the Baby Boomers reaching retirement age) and encourages higher consumer spending and debt.

A decade and a half of near-zero interest rates did exactly that, exacerbated by regulatory strangulation and energy-cost increases committed by the federal government distorting investment choices. These factors and others reduced the personal saving rate, increased consumer debt, and moved investment money from its most reliable and desired uses to more-speculative ones (and in general away from “hard” things such as manufactured goods, which cost more to get started, and toward “soft” things such as services and intellectual property, which are more easily ramped up and down as conditions change). The stock markets and homeowners benefited, while others struggled.

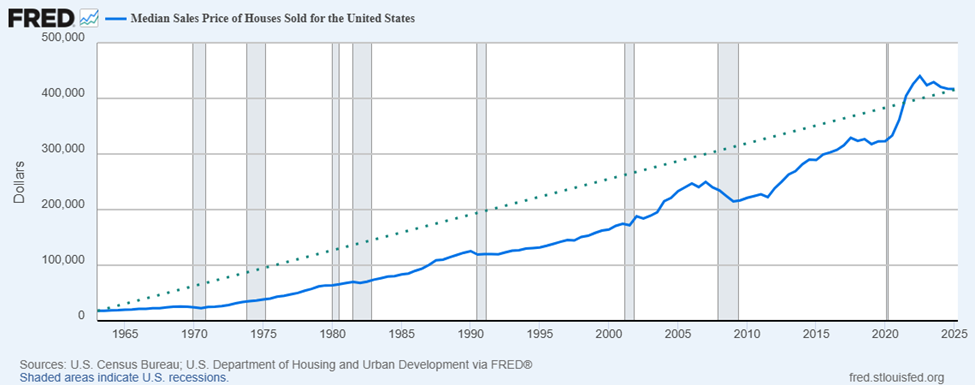

Consider the effect on the housing market. Housing prices have risen rapidly ever since President Richard Nixon disconnected the dollar from gold in the early 1970s, and the price increases have been especially pronounced since 1990 as localities have tightened restrictions on building and development, especially in large urban areas:

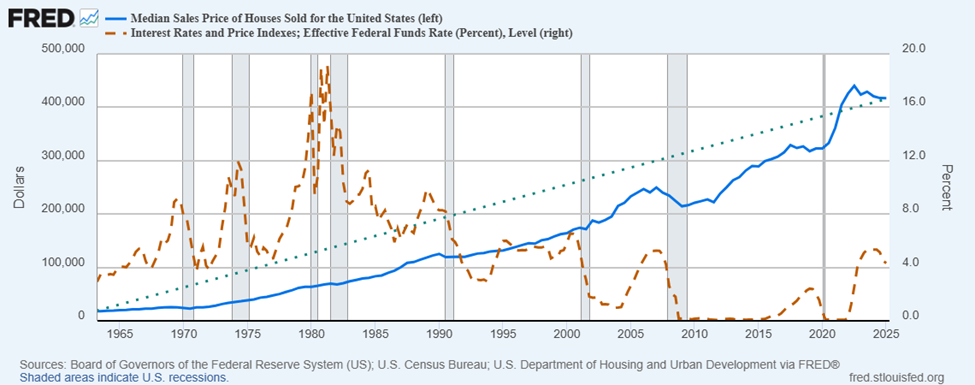

Rapid decreases in the fed funds rate from somewhat normal to near-zero have preceded outsized increases in housing prices in the current century:

“The fact that we hit record high home prices is reflecting multiple years of undersupply,” The Wall Street Journal quotes Lawrence Yun, the National Association of Realtors’ chief economist, as saying. High prices plus high interest rates have made it difficult for buyers and sellers to come to terms:

Home buyers were hesitant to jump into the market this spring, which is usually the busiest time of year for home purchases. Home sales in June fell to a nine-month low. Home prices at record highs, along with mortgage rates above 6.5%, have made home purchases unaffordable for many.

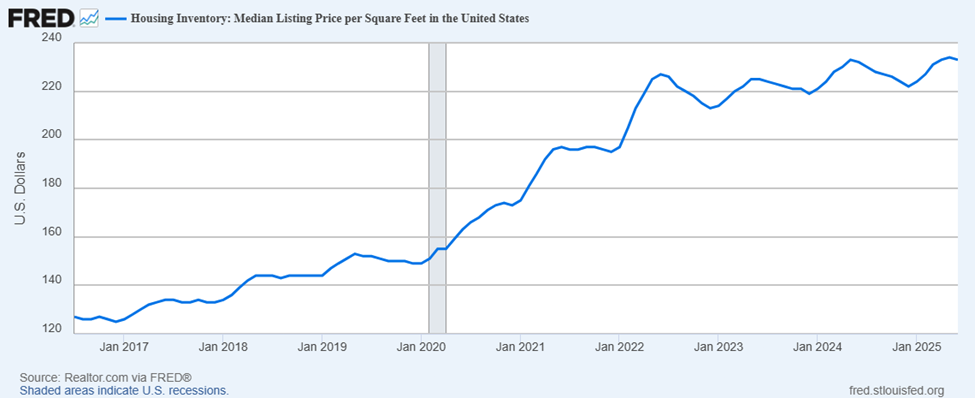

The price increases have not been caused primarily by newer homes being bigger; quite the contrary, in fact:

The trouble in the U.S. housing market shows how unduly high interest rates can suppress economic activity.

Money is information: it tells us the relative values people place on goods and services. In so doing, it enables people to distribute their resources—time, money, labor—to the endeavors that will create the most value. That information becomes distorted—in fact, falsified—when a central bank or any other factor manipulates the cost of money. It is difficult to know what is the ideal interest rate. That is why that decision is best left to the market to decide, instead of government. (Pegging a currency to gold, which rises at a steady rate of 2 percent per year, would remove central banks’ monetary distortions.)

The Fed has used high interest rates and asset sales to tighten the money supply for three years now and is reluctant to change that, in particular by lowering the fed funds rate. (It is still selling assets, another means of reducing the money supply). The central bank watched inflation soar during the Biden administration and wants to ensure that it does not recur. The board’s governors fear inflation more than recession, perhaps because inflation affects everybody and recessions mainly hit those who lose their jobs. It’s a good working hypothesis, anyway.

The Fed caused the 2020s inflation by monetizing the Biden-Harris administration’s massive, irresponsible increase in the federal deficit and debt. The budget has stabilized now, however, with the federal government surprisingly running a slight surplus in June. That will undoubtedly prove temporary, but the lower-deficit trend will sustain as long as economic growth continues and Congress does not increase spending any further: rising growth raises tax revenues.

As I write, the current effective fed funds rate is 4.33 percent. That is much higher than it has been at any other time in the 2000s, except for the run-up to the Great Recession of 2008:

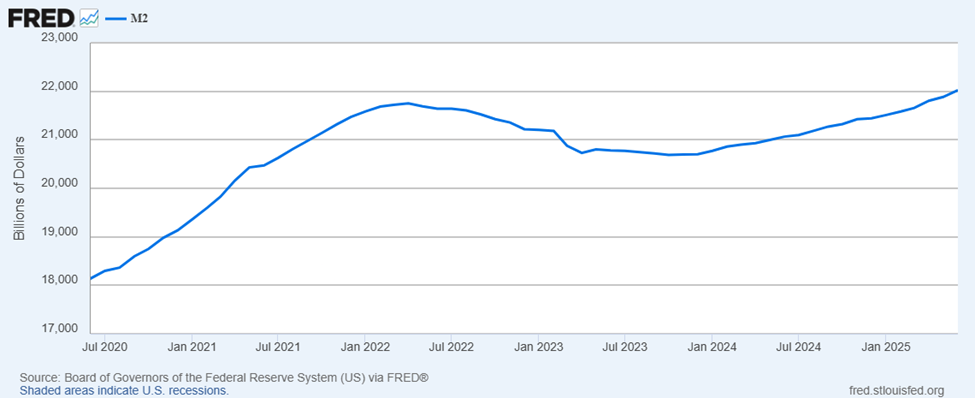

The latter fact suggests that the current fed funds rate is too high, and the percent change in the money supply affirms that conclusion, as recent money supply growth has been lower than normal:

All of this suggests that the Fed should reduce interest rates—gradually and with a keen eye monitoring the situation—to give the economy room to expand further and take advantage of improved federal fiscal, regulatory, and energy policies. Though federal fiscal policy still needs serious reform—through substantial cuts in spending—squeezing the economy via tight money is certainly not the solution to our economic problems.

Ever wonder what happens when political spin meets reality? It’s like watching a magician whose tricks have been exposed – suddenly everyone can see the wires!

• 🎭 In this explosive episode, we’re serving up a feast of political commentary that’s more satisfying than whatever’s NOT rotting in Kansas City’s taxpayer-funded grocery experiment.

• 🎯 Obama’s Russia-gate narrative gets the fact-check it deserved years ago

• 🎪 Hunter Biden’s media circus tour – damage control or career suicide?

• 🏪 Socialist grocery stores: when ideology meets produce sections

Socialism on the Rise in Northern Cities

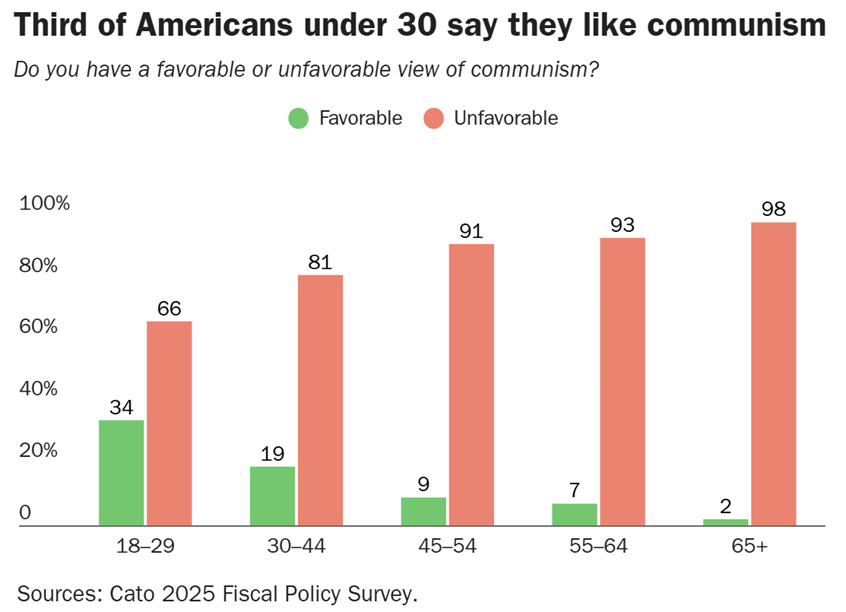

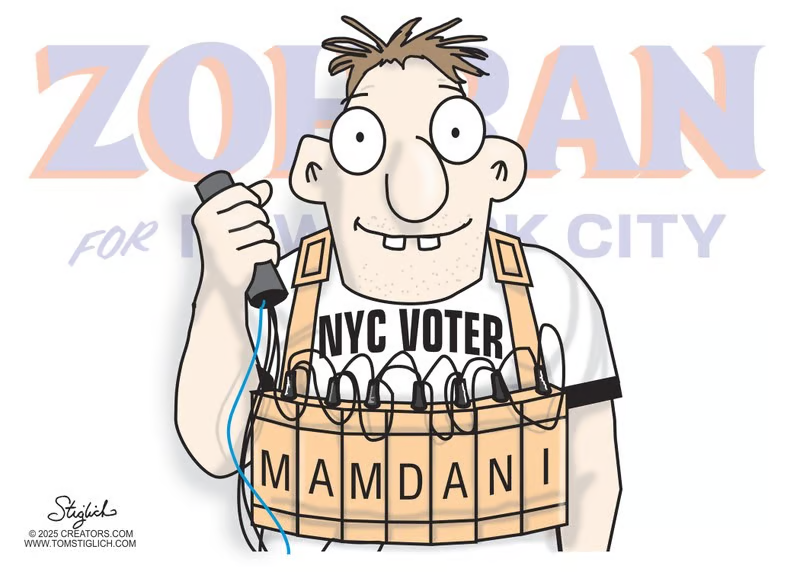

With avowed socialists Zohran Mamdani and Omar Fateh winning the Democratic Party endorsements for mayor in New York City and Minneapolis, respectively, it might appear that socialism is on the rise. A Cato Institute/YouGov poll released in April found that 62 percent of Americans under the age of 30 feel favorable toward socialism, and a startling 34 percent said they view Communism positively:

Less than 1 in 5 Zoomers were proficient in history when they were in the 8th grade, according to NAEP reports. If they had even a basic understanding of history, surely they’d know of the 100 million plus lives communism claimed in the 20th century through unimaginable hardships in Soviet gulags, Chinese repression and famine and genocidal regimes such as the Khmer Rouge in Cambodia.

“Fiscal illiteracy” adds to young people’s lack of discernment about communism and socialism, the Post reports:

The majority of Gen Z is fiscally illiterate, and their “functional knowledge is substantially lower for each area compared with older generations,” according to the 2025 TIAA Institute-GFLEC finance and retirement report.

Still, these young people have the vote, so they may get what they want.

However, what they get after they get the politicians they want might not be quite what they were hoping for. Britain’s socialist Labour government is chasing out highly wealthy people who emigrated to the island nation to avoid high taxes elsewhere. The Wall Street Journal reports,

The U.K. is trying to tax the superrich. It’s off to a bumpy start.

“I’m on my way out,” said Bassim Haidar, a Nigerian-born Lebanese businessman who moved here in 2010. “There comes a time when you don’t feel welcome anymore, and it’s time to just start packing and leaving.”

Haidar is one of the estimated 74,000 who used a centuries-old tax loophole, abolished in April, that catered to the global rich. The nondomiciled—or non-dom status, as it is known—allowed foreigners living in the U.K. to pay tax only on what they earned domestically. Profits made abroad were ignored unless brought into the U.K.

Beset by high public debt and crumbling infrastructure, the U.K. hoped eliminating non-doms would bring in about $45 billion by 2030. But instead of paying up, wealthy expats are rushing for the exits, sparking questions about whether the effort will raise any money at all.

The answer to that question is easy to see: the big new tax on ultra-wealthy, highly mobile immigrants will be a money loser.

That is precisely what Mamdani proposes to do in New York City, the WSJ article notes:

In the U.S., New York City Democratic mayoral nominee Zohran Mamdani has proposed a “millionaires tax” on New Yorkers making more than $1 million a year, prompting vocal rich people to say they will leave for lower-tax jurisdictions such as Florida or Texas.

The wealthier your tax target, the less likely you are to pin it down. The WSJ reports:

One challenge of taxing the wealthy is that they are highly mobile, with houses around the world, private jets and an army of advisers who can sort out visas and bureaucratic paperwork quickly. Jurisdictions such as Dubai, Italy and Monaco have rolled out the red carpet, offering no taxation or structures similar to the U.K.’s old non-dom status. …

The U.K. always knew that some rich residents would leave because of the tax changes and built that into its forecasts. The U.K.’s independent budget watchdog, the Office for Budget Responsibility, estimated that among a large subset of non-doms, around 12% will move. But it warned this month that departures could be higher and said the U.K.’s “growing reliance on this small and mobile group of taxpayers therefore represents a fiscal risk.”

Campaign groups that back lower taxes paint a gloomier picture. A report from the Centre for Economics and Business Research, commissioned by the Land of Opportunity campaign, forecast that a higher share of non-doms would leave and suggested the government could lose money if the migration rate tops 25%.

The wealthy change their residences and move their money when taxes get too high. The government then lays those tax obligations on regular working people, as they never consider cutting spending. The working people pay the price of the government’s stupidity and lust for power.

People in the United States have the option of moving to different places within the country where the governments treat the public less vampirically. They have been doing so throughout the current century.

Working people in New York City, Minneapolis, and other cities may soon receive powerful further encouragement to join the exodus.

The International Court of Justice at the United Nations this week ruled that failing to take poverty-creating “appropriate action to protect the climate system” — meaning ending the use of life-giving fossil fuels — could open nations to being hauled before a global tribunal to answer for their crimes. As a trio of climate attorneys wrote in The New York Times, “continuing fossil fuel production and use, let alone expanding it, violates the law.” We’ll see about that.

Contact Us

The Heartland Institute 3939 North Wilke Road Arlington Heights, IL 60004 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org