Life, Liberty, Property #131: The Fraud Is Worse Than You Ever Imagined

Forwardthis issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

IN THIS ISSUE:

The Fraud Is Worse Than You Ever Imagined

Video of the Week: Why Socialism Is Evil: The Moral Case Against Collectivism

Trump’s Homeownership EO

The Fraud Is Worse Than You Ever Imagined

U.S. taxpayers have been victimized by at least $36 billion and possibly as much as $3 trillion in fraud through federal government entitlement programs since 2020, an investigative report by The Center Square states. The higher number is far more than most sources have suggested in the past.

The news agency’s review of “all the statements about entitlement fraud cases issued by the U.S. Department of Justice from 2020 to last year” shows that “public safety net programs such as Social Security, Medicare, and Medicaid lost billions of dollars to scams each year,” investigative journalist Mark Stricherz reports. “The amount ranged from $2.7 billion in 2022 to $14.5 billion in 2025,” Stricherz writes.

The U.S. Department of Justice (DOJ) announced “convictions, guilty pleas, and sentencing” in nearly 300 cases totaling $36 billion from 2020 through 2025, Stricherz reports. The 2,500 DOJ statements, press releases, and fact sheets The Center Square reviewed “did not include many of the cases prosecuted by U.S. Attorney’s offices in the various districts and any state prosecutions,” suggesting a far greater scope of fraud than what the investigation identified directly, Stricherz reports:

Fraud experts said, if anything, the $36 billion figure is too low.

“The number doesn’t surprise me,” said Linda Miller, president and co-founder of the Program Integrity Alliance, an independent 501(c)(3) nonprofit, nonpartisan organization that seeks to strengthen government integrity through data, evidence, and public-sector innovation. “That’s fraud that has been identified and investigated, so it represents a fraction of the actual fraud that has occurred or is occurring. Fraud is deceptive, and most agencies lack the tools to proactively prevent it, meaning the actual amount of fraud is much higher.”

The amount of fraud is surely in the hundreds of billions of dollars per year, American Enterprise Institute Senior Fellow Matt Weidinger told The Center Square, Stricherz reports:

He cited a 2024 U.S. Government Accountability Office report concluding that, based on data from 2018 to 2022, the federal government is defrauded of $233 billion to $521 billion annually. While the report examined federal spending overall, Weidinger noted that “entitlement programs constitute the bulk of federal spending and presumably fraud, too.”

The DOJ documents suggest fraudsters hit Medicare and Medicaid the hardest, Stricherz reports:

In the first half of last year alone, the agency announced that it had identified and investigated approximately $14 billion in fraud in the two federal health care programs, as well as Tricare, the health care program primarily for active-duty military, retirees, and their families.

The DOJ documents suggest that the amount of fraud rose rapidly between 2020 and 2025, Stricherz reports: “The figure [for the first half of the year for Medicare and Medicaid] is more than twice the $6 billion in fraud to federal health programs that the Justice Department identified in September 2020.”

Stricherz documents several cases in which medical professionals defrauded the federal government for literally hundreds of millions of dollars apiece.

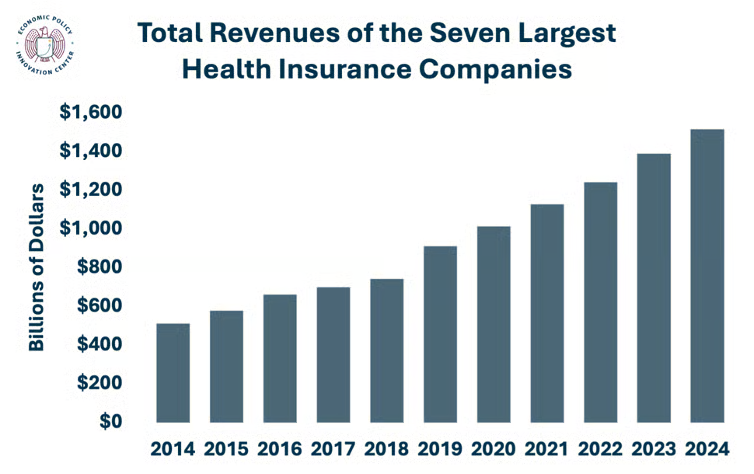

The impact of fully legal rip-offs may be even worse. Insurance companies have received a huge windfall in the past dozen years, with revenues tripling in a single decade since Obamacare went into effect. The Unleash Prosperity Hotline reports,

The Left has fallen in love with the insurance conglomerates. They may throw some punches at the big insurers, but that’s for show.

The only health care bill Democrats have voted for—over and over—is one that shovels even more tax dollars to these insurers with zero reforms. …

The source of the Hotline graph and data notes that those companies are amassing great wealth through the Obamacare subsidies: “The stock prices of the health insurance companies have soared at an even higher rate than their revenues, outpacing the S&P 500,” wrote Gadai Bulgac for the Economic Policy Innovation Center last month.

This many-headed health care entitlement system assembles an enormous and powerful coalition of business interests, benefit recipients, and politicians, making it extremely resistant to accountability and reform that could reduce the burden on taxpayers while providing better help to the truly needy. It is a gigantic scam that generates ever-increasing corruption and cannot do otherwise.

The supposedly shocking revelations of entitlement fraud in Minnesota and the subsequent reports of possibly hundreds of billions of dollars ripped off from government “safety net” programs should surprise no one. The very design of Medicaid, for example, rewards theft and invites corruption. The dual-funding structure, with the federal government providing the vast majority of the money, enables states to make money by allowing ineligible people to draw benefits.

… [S]tates like California are quietly siphoning off billions in federal Medicaid dollars through legalized budget fraud tied to the Intergovernmental Transfer loophole.

It works like this: State-run hospitals or county agencies send funds to the state Medicaid program. The state counts those as its own Medicaid spending, uses them to trigger a higher Federal Medical Assistance Percentage match from the federal government, and then sends most of the money back to the local provider—often with a bonus.

No new services are delivered. No patients are helped. But billions in federal money change hands—and California is the poster child for using this racket to cover its budget gaps. …

That is just one of many ways that states can steal from other states’ taxpayers by taking advantage of perverse Medicaid rules and lax enforcement by the federal government.

The dual-funding system corrupts state and local governments, greatly increases inflationary federal deficit spending, transfers hard-earned taxpayer money to less-worthy recipients and outright thieves and grifters, unfairly enriches insurance companies and unscrupulous health-care providers at taxpayer expense, fosters economic crimes such as kickback schemes and false or exaggerated claims of service provision, rewards wasteful-spending politicians with big campaign contributions, and undermines the credibility of all levels of government, among countless other deleterious effects.

Congress has known about all this “legalized budget fraud” for years and has consistently refused to end it. As I have regularly observed, the only real reform for this system would be for the federal government to eliminate the dual-subsidy approach and remove the program’s third-party payment mechanism.

That would mean converting the federal government’s financing into block grants and requiring the states receiving that taxpayer money to pass it directly to recipients (through health savings accounts) for them to pay to providers directly, fostering competition throughout the system and forcing the health care industry to adopt true price transparency because patients will demand it.

Vitally, this fundamental reform would also mean requiring the states to enforce federally established eligibility requirements or have their grants reduced by more than the amount of any fraud they fail to report (to make the states pay for their own transgressions), which the federal government should ascertain through database comparisons, whistleblower rewards, investigative “stings” of suspected violators, and the like.

The latter investigations would be directed at state and local governments and health care providers receiving patients’ payments, not the patients themselves unless those individuals are committing crimes such as double-dipping, kickbacks for work not done, lying about eligibility, and the like. No one should pay for work not delivered, and that should apply to taxpayer money most of all (because it is taken by threat of force), whereas today taxpayer protection is consistently the last thing most governments seem to think about.

Only the truly needy should receive public benefits, and measures such as time limits and work incentives ensure that those relying on their neighbors’ dollars truly need the help. Ginn agrees:

The real path forward is not more subsidies, whether via the Affordable Care Act or Medicaid. It’s structural reform.

We should start by shutting down Intergovernmental Transfer abuse—ending circular transfers, enforcing transparency in Medicaid financing, and tying federal dollars to real services delivered to real patients.

Then we need to empower patients directly. In myEmpower Patients Initiative with Dr. Deane Waldman, we propose giving Medicaid recipients no-limit Health Savings Accounts, funded through state block grants. These accounts allow individuals to pay providers directly, shop for care, and make health care decisions on their terms.

Paired with time limits and work incentives for work-capable adults, this model would reduce dependency, lower costs, and improve outcomes. It would also inject long-overdue competition and price transparency into a system that’s been shielded from both.

The nation’s entitlement system is entirely corrupt. That is obvious. The truly constitutional response would be to kick all these programs down to the state level with no federal spending at all, no oversight, no regulation, no nothing. The Constitution does not authorize any of these programs, and the appalling state of the federal entitlement system proves the founders’ wisdom in leaving this to the states.

Of course, a return to constitutional government in that regard is not going to happen, short of a collapse in the federal government’s borrowing ability, which is in fact likely to occur within the next seven or eight years unless the federal government implements the type of major entitlement reform I am recommending. More than 74 million Americans received entitlement money in 2025, and businesses and politicians reap benefits from all this spending. Nobody is eager to give that up.

The choice, however, is to reform it now or lose it all in a few years.

In this powerful presentation from The Heartland Institute’s World Prosperity Forum in Zurich, Switzerland, Donald Kendal, director of the institute’s Emerging Issues Center, explains why socialism isn’t just an economic failure—it’s a fundamentally immoral system that destroys individual freedom and conscience.

Trump’s Homeownership EO

Upon hearing that the president of the United States has implemented an executive order titled Stopping Wall Street from Competing with Main Street Homebuyers, the first thing that comes to mind for any proponent of individual rights and limited government is that it is a very bad idea. Although housing affordability is certainly a serious problem, “stopping” people from “competing” with one another is no way to reduce prices for the consumer.

The very opposite is true, of course. In addition to the economic incoherence of such a position, it seems a classic case of executive overreach.

Pointing out that a central element of the American Dream is home ownership, Trump makes an important point that I have noted regularly: that the current housing affordability crisis is an acute, short-term problem caused by bad recent government policies, specifically massive increases in federal spending unleashed during the first two years of the Biden administration, on top of a long-term housing supply deficit caused by government regulation and a huge population increase caused by mass immigration. Trump writes,

… because of the recent high inflation and interest rates caused by the previous administration, that American dream has been increasingly out of reach for too many of our citizens, especially first-time homebuyers.

That is accurate and is sound economics. Trump then turns to the issue of competition, which he considers from the demand side of the price equation:

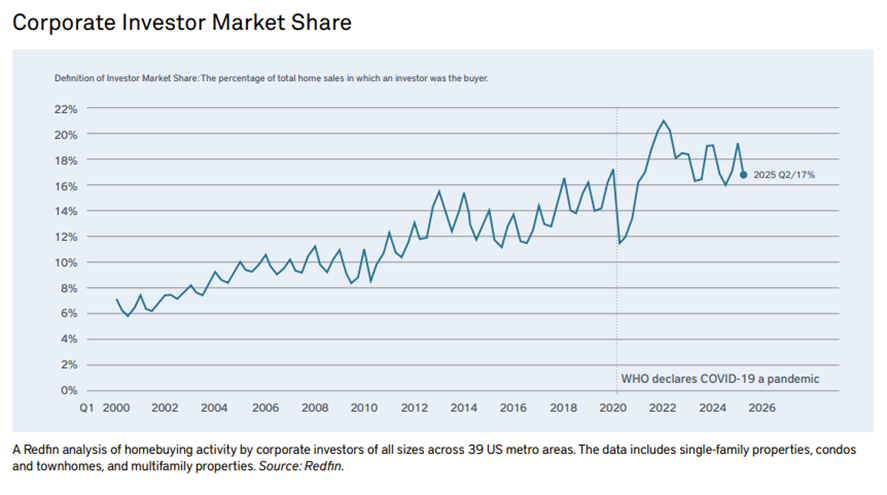

At the same time [as inflation and rising interest rates pushed up home-buying costs], a growing share of single-family homes, often concentrated in certain communities, have been purchased by large Wall Street investors, crowding out families seeking to buy homes.

… [D]ata suggests that investors made nearly one-third of the country’s single-family home purchases in the first half of 2025— buying roughly 85,000 properties a month (Cotality 2025). In 1991, according to the US Census, individual investors owned 92 percent of rental properties (US Census 1996). By 2021, that figure had dropped to 73 percent (Hermann 2023).

Corporations’ share of home purchases in the United States has more than doubled since the year 2000, the study states:

With all that corporate demand competing for houses and pushing up prices, “record numbers of households are now cost-burdened, spending more than 30 percent of their income on housing (Joint Center 2025),” the report states.

Trump’s EO summarizes those insights as follows: “Hardworking young families cannot effectively compete for starter homes with Wall Street firms and their vast resources.”

That, too, is accurate, as the above-cited data confirm.

Still, none of this makes an economic case for the government to intervene in the market, nor a constitutional case for the president to do so on his own initiative. Trump, however, generally confines his order to a course of action appropriate in both regards: stopping federal agencies from directly participating in corporations’ purchases of residential property:

Sec. 3. Restrictions on the Sale of Single-Family Homes by the Federal Government. (a) Within 60 days of the date of this order, the Secretary of Agriculture, the Secretary of Housing and Urban Development, the Secretary of Veterans Affairs, the Administrator of General Services, and the Director of the Federal Housing Finance Agency, as appropriate, shall issue guidance to:

(i) prevent agencies and Government-sponsored enterprises from engaging in the following, to the maximum extent permitted by law:

(A) providing for, approving, insuring, guaranteeing, securitizing, or facilitating the acquisition by a large institutional investor of a single-family home that could otherwise be purchased by an individual owner-occupant; or

(B) disposing of Federal assets in a manner that transfers a single-family home to a large institutional investor; and

(ii) promote sales to individual owner-occupants, including through anti-circumvention provisions, first-look policies, and disclosure requirements.

Those directives are defensible as limitations on damage the federal government has been doing and an attempt to remove government-devised market distortions. Trump also orders federal housing program administrators to find out who owns the homes that taxpayers are helping to pay for:

The Secretary of Housing and Urban Development shall, to the maximum extent permitted by law, require owners and managing agents of single-family home rentals participating in Federal housing assistance programs to disclose to the Department of Housing and Urban Development direct or indirect owners, managers, or affiliates, including changes in ownership or control of single-family rentals, to the extent necessary to determine any involvement of large institutional investors.

Preventing big corporations from driving up the cost of federally subsidized housing is a reasonable requirement, though all these programs are in themselves unconstitutional and economically harmful, in my view. If the programs are going to exist, however, the government should at least try to make them less destructive, as this directive is intended to do.

Two other provisions of the EO are problematic at best, however. First, the president expands antitrust action into this area:

The Attorney General and the Chairman of the Federal Trade Commission shall review substantial acquisitions, including series of acquisitions, by large institutional investors of single-family homes in local single-family housing markets for anti-competitive effects and prioritize enforcement of the antitrust laws, as appropriate, against coordinated vacancy and pricing strategies by large institutional investors in local single-family home rental markets.

I am not a fan of antitrust laws at all. Antitrust basically amounts to governments grabbing additional power to deal with problems it previously created through its own interference, imposing further restrictions on the market in response to the damage it has already done. It is a thoroughly bad idea.

However, it is important for presidents to enforce the laws as written and intended. This provision is clearly aimed at that, so it’s justifiable because we have antitrust laws and are stuck with them for the foreseeable future. The president does not have the authority to ignore these laws altogether, and doing so would only leave in place the damage caused by the laws and regulations that led to the problems the antitrust actions are meant to remedy.

Trump then directs his team to develop legislation for Congress to consider legislation that would give his EO force of law and make it impossible for a future president to reverse without congressional approval:

The Deputy Chief of Staff for Legislative, Political and Public Affairs shall prepare a legislative recommendation to codify the policy set forth in section 1 of this order so that large institutional investors do not acquire single-family homes that could otherwise be purchased by families.

That is the right way to implement policy changes. Ironically, it is the one thing in the executive order that is truly worrisome. The federal government should not be interfering in the housing market. Its countless interventions have led to the very problems Trump is trying to solve in the executive order. New legislation of the sort Trump is calling for would be additional government overreach. It would surely create new problems, which a later government would “solve” with even more restrictions on our inalienable property rights, which are always getting more alienated.

Government intervention does not remedy government intervention. Only government retrenchment can do that: removal of the bad laws that are causing the problems.

I know: there’s no chance that any Congress and any president will voluntarily rescind the myriad laws that have created all these market distortions, nor that they will rein in the central bank’s monetary manipulation that makes everything even worse. New laws, however, will only increase the governmental distortion of the nation’s economy and further reduce the affordability of the most desirable goods and services.

The only way for the federal government to solve our problems is to stop creating them.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org