Life, Liberty, Property #149: Federal Reserve Assumptions Have to Change

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

In This Issue:

Federal Reserve Assumptions Have to Change

Video of the Week: Social Security Insolvency by 2032 – In The Tank #540

Could Entitlement-Fraud Recovery Help Save Social Security?

Medicaid’s Economic Damage Explained

Hot off the Presses!

‘Today’s crisis is a product of government errors, not greedy landlords, institutional investors, and so-called market failure.’

Federal Reserve Assumptions Have to Change

The Consumer Price Index rose by 4.2 percent year-over-year in May, the Bureau of Labor statistics announced in its inflation report released on Wednesday. That is more than double the Federal Reserve’s goal of 2 percent annual increases in the price index.

The Producer Price Index (PPI) showed annual inflation at 6.5 percent.

Higher oil prices drove the price increases as the closing of the Strait of Hormuz reduced the global supply of petroleum. That effect was widely expected, and it will prove temporary once the newly announced peace deal with Iran unblocks the flow of oil from the Middle East and replenishes world supplies.

The inflation numbers arrived as the Federal Open Market Committee (FOMC) was preparing its interest rate decision for this Wednesday. The Federal Reserve (Fed) has been reluctant to reduce interest rates, which would stimulate the economy, while inflation is above target.

Some FOMC members have publicly called for a rate hike, which would reduce economic growth and possibly move the economy dangerously close to a recession.

As the government-created central bank responsible for keeping prices and employment stable, the Fed should always make sure to identify long-term trends and not get too worried or elated over monthly numbers. The worrying is for Wall Street, the press, and the public to do.

With that in mind, new Fed Chair Kevin Warsh has proposed paying more heed to trimmed-mean averages: an inflation measure that strips out items with more-volatile prices as a way of identifying underlying monetary trends rather than faster-moving costs of consumer and producer baskets of purchases.

The Core CPI was 2.9 percent in May, well below the 4.2 percent for the CPI. Core PPI came in at 4.9 percent in May, the same as in April and a half of a percentage point below economists’ expectations. That is very high but nothing like the 6.5 percent the PPI showed.

The idea behind the use of trimmed-mean averages is to focus the Fed’s attention on the overall effects of its changes in the money supply. There is no perfect measure of the effects on the economy that the central bank creates through its policy choices in managing the money supply. That is a powerful argument for using an outside monetary standard (such as gold or a fixed basket of important commodities) or allowing the market to decide currency values exclusively.

Tying the money supply to something real such as gold would solve the inflation and economic boom-bust cycles. The same is true of allowing the market to create money.

The problem is that past gold-backed currency regimes have not always been able to prevent liquidity crunches, widespread bank failures, and the like. Those, however, can remain short-term problems that will correct fairly promptly if governments do not intervene. Unfortunately, governments seldom resist the temptation to wade in with supposed solutions that make things worse.

The Federal Reserve System, however, has regularly and often spectacularly failed to achieve its assigned objectives of establishing monetary stability, averting financial crises, and fostering a strong, market-based economy. Instead, it has created crises and continual instability, greatly to the detriment of the U.S. economy and the welfare of the American people. Things have gotten worse and worse since President Richard Nixon severed the last ties between the U.S. dollar and gold in 1971.

The current U.S. economic situation is exactly that: current. Individual and group fortunes rise and fall continually as circumstances change with the vagaries of chance, happenstance, bad government policies, and economic fads and enthusiasms. True prosperity depends on steady efficiency in the production of goods and services: long-term trends and hard realities. Warsh has the right idea for the nation’s central bank.

The Social Security trustees predict the retirement trust fund is now projected to run dry a full year earlier than previously forecast, in just 2032. What got us here, and what does Congress need to do about it? Can we keep pushing insolvency forward forever? And: where does good government end and dangerous negligence begin? The Belfast riots are the latest example of a Western government that suppressed legitimate debate about immigration and crime, and now things are boiling over.

Finally, related to our main topic but separated by over 250 years: the Intolerable Acts of 1774 pushed the colonies past the breaking point, despite an attempt at reconciliation in the Olive Branch Petition, which King George ultimately refused to even read.

The Heartland Institute’s Linnea Lueken, Jim Lakely, S. T. Karnick, and Chris Talgo will talk about all of this and more on Episode #540 of the In The Tank Podcast.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Could Entitlement-Fraud Recovery Help Save Social Security?

The Social Security Administration announced last week that the Old-Age and Survivors Insurance trust fund will run out of money in late 2032. The government will no longer be able to pay retirees their full promised benefits at that time.

The new date is earlier than previously expected: the deadline has been moving steadily closer to the present as revenues fall short of the government’s projections. The Medicare trust fund will run out of money in 2033, as well.

This is a rapidly approaching crisis for retirees, prospective retirees, taxpayers, the government, the U.S. economy, and recipients of federal welfare benefits. When the Social Security trust fund runs out of money six years from now (or earlier), the projected income from payroll taxes will cover only 78 percent of promised benefits. The government will have to borrow more money, reduce benefits, raise taxes, extend the retirement age, and/or cut other spending. Most of those options would be inflationary, recessionary, or both.

The draining of the Social Security trust fund is a short-term crisis that has arisen from a long-term problem, as is the case with so many of our nation’s current troubles.

The program’s trustees said revenues are less than expected because of last year’s reduction of the tax on Social Security benefits, plus declining fertility rates and lower immigration. The real cause of the problem is the aging of the nation’s population, as our working people have to support a rising number of retirees. That is not going to change, yet Congress and presidents have refused to confront the truth.

Financing retirement requires just one thing: saving. The federal government has been borrowing against the Social Security trust fund for years, spending it on current largesse to buy votes from various population groups. Even so, the government has been running big deficits. A massive reduction of federal spending on items other than Social Security and Medicare could reduce or eliminate the shortfall. That, however, seems politically impossible.

A major sticking point for any Social Security and Medicare reform is that these are programs for which the federal government took money from workers and employers and promised to save it for those workers’ future retirement needs. Instead, the government added additional benefit classes and, as the Baby Boom generation created large surpluses in the system anyway, the federal government spent that money on other things and put IOUs in the trust fund.

In addition, Social Security pays much more poorly for retirees than private investment would have done, and the workers were given no choice about whether to pay in. Failure to keep this basic promise to the nation’s workers would greatly undermine the U.S. government’s credibility (which is already abysmal) and endanger the Treasury’s ability to borrow money. That would hike interest rates and create a recession while sparking inflation: a classic stagflation scenario.

Given those hard constraints, the only way to avert a Social Security doom spiral is for the government to patch the entire entitlement system right now by reducing Social Security benefits, increasing economic growth through lower tax rates and less regulation, and cutting spending significantly on other entitlement programs and national security “wants” as opposed to needs.

There is, however, a sliver of hope. This may be a uniquely good time to begin the discussion in earnest, as the revelations of astonishing levels of fraud in the nation’s entitlement programs provide a strong political opportunity for reform.

Eliminating the fraud in those programs could save hundreds of billions of dollars a year, according to what may well prove to be conservative estimates.

Congress and the president could make a very persuasive and truthful argument to the American people: every dollar saved by fraud reduction would be set aside specifically for Social Security and Medicare, under force of federal law, to relieve the coming spending crunch. The Baby Boomers would be all-in on that, and they vote. So would anyone who disapproves of fraud.

Another way to ameliorate the upcoming shortfall would be to resume extending the minimum retirement age, a process that ended this year. The average American now lives to the age of 77 and becomes eligible for minimum Social Security benefits at age 62 and full benefits at 67. In 1935, the average American who reached adulthood could expect to live to around 65 years, the minimum age for Social Security benefits at the time.

Increasing the retirement age by one year each year through 2033 is an essential change, even if unfortunate and jarring for those who are expecting to retire soon. It would add workers and decrease costs. Those who will have to delay retirement by a year will probably prefer that over 22 percent benefit cuts in perpetuity or a fiscal collapse of the federal government that could zero out their benefits altogether.

The federal government has known for many years that the retirement system is unsustainable. The trustees’ report is just another reminder of this reality. Using fraud recovery to shore up Social Security and Medicaid would be a historically important deal and could save the nation from a fiscal calamity.

Although it would not solve the problem on its own, fraud recovery could make a full solution possible. Without such a plan, a repudiation of major federal obligations is almost inevitable, followed by a full collapse of the government’s credibility and its ability to maintain rule of law.

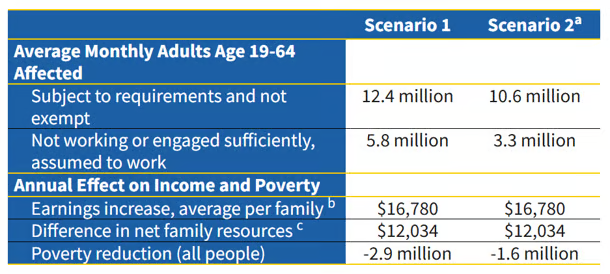

We analyze two scenarios, with details presented in the Table. Scenario 1 assesses the full potential reach of the benefits by including the entire Medicaid-eligible population, assuming all eligible adults enroll, and immediately find adequate employment to meet the requirements. It also assumes states face no implementation challenges. Under Scenario 1, in an average month, 5.8 million adults would be subject to the requirements, and if they all worked in the months they would otherwise have lost Medicaid, they would see an average net income increase of $16,780 per family. This would lead to 2.9 million fewer people in poverty annually.

Scenario 2 adjusts for factors that could impede the potential reach of this policy, as formulated by the Urban Institute. It also considers that around 85 percent of eligible adults actually enroll in Medicaid, and assumes that not everyone will easily find work, proxied by the employment rate for the population in poverty (rounded to 80 percent based on the 2025 Current Population Survey, Annual Social and Economic Supplement). Even under Scenario 2, 3.3 million adults would still increase work to comply in an average month, and 1.6 million fewer people would be in poverty annually.

Table. Economic Impact of Medicaid Community Engagement Requirements, Steady-State Estimates

The analysis shows that “Medicaid work requirements can take 1.6 to 2.9 million people out of poverty,” the study found:

Our review of the past literature found that work requirements increased long-term employment (up to 5 years) by 4.2 percentage points. We calculated that Medicaid work requirements included in the Working Families Tax Cut of 2025 could increase family net income by $12,034 and reduce poverty by 1.6 million to 2.9 million, thereby promoting economic mobility and strengthening labor force participation.

Enforcement of the rules is critical, as is encouragement of free markets within each state, the report notes:

As with any policy intervention, benefits are contingent on how states implement the requirements. However, the key takeaway is that if implemented appropriately and with enough employment opportunities, these requirements could increase work and overall earnings among Medicaid recipients subject to them.

To reach such outcomes, implementation of work requirements is crucial. States can consider pairing work requirements with other services, such as job training, and ensuring verification processes are streamlined. Primary care clinics and community pharmacies can also support work verification. In the meantime, pro-growth economic policies must occur simultaneously to ensure job availability. For example, Medicaid recipients with basic or minimal job training would face significant challenges in jurisdictions that require high minimum wages and impose restrictive licensure requirements. Policymakers interested in promoting work and reducing poverty must consider effectively implementing both incentives that increase labor supply, such as Medicaid work requirements, and those that stimulate organic, market-oriented demand from employers.

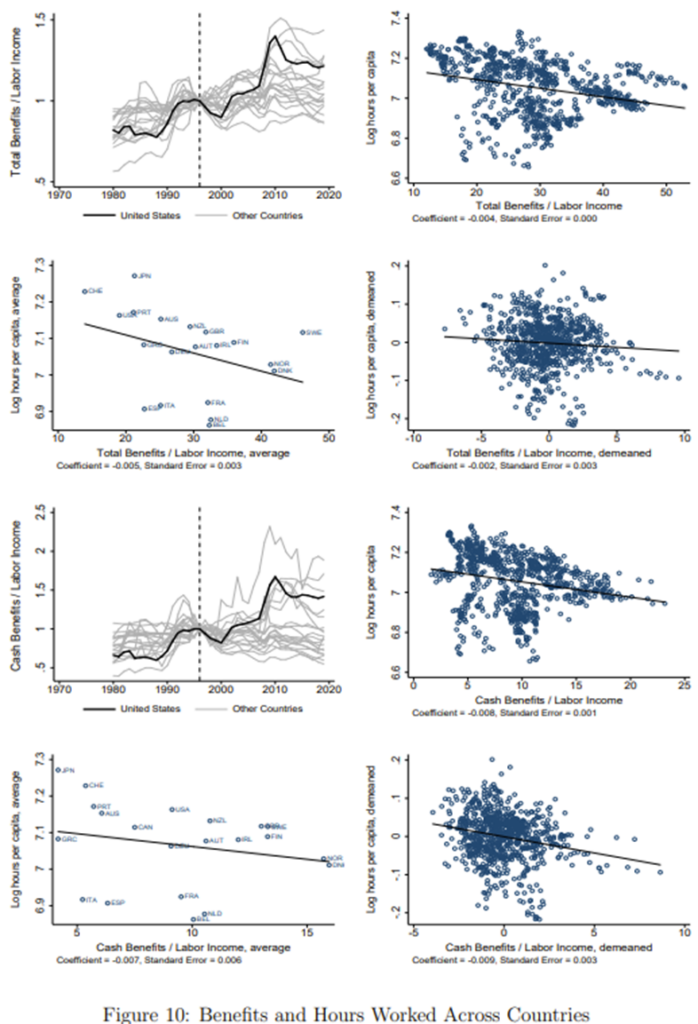

The HHS report cites a recent study by the National Bureau of Economic Research (NBER) which found “the number of hours worked per person in the U.S. has declined over the past couple of decades.” The NBER study, published in April, reports the United States has lost its advantage in labor force participation over other nations in the past quarter-century.

“Americans no longer work so much more than non-Americans,” the study states. The main cause is the explosive increase in public health benefits, especially Medicaid, the researchers found:

Our main finding is that U.S. hours per person declined after the 2000s owing to the rise of benefits provided to the non-employed. Among these benefits, we find the most important role for health benefits and, in particular, Medicaid. According to the official Medicaid and CHIP Payment and Access Commission (https://www.macpac.gov/), the number of Americans on Medicaid increased from roughly 20 million in the early 1970s to almost 100 million in the early 2020s. In our model, the increase in benefits mainly distorts the extensive margin of labor supply, as it raises the value of not working. While historically, non-U.S. countries offered more generous benefits for the non-employed, this generosity has not changed as much over time as in the United States, and core public health coverage does not depend on employment status or income levels. For non-U.S. countries, the increase in labor supply is generally accounted for by a combination of a rise of wages, a falling disutility of work along both margins, and in some cases changes in benefits, but no single factor stands out as prominently as the rise of health benefits in the United States. The rise in hours due to a falling disutility of work in non-U.S. countries is consistent with the U.S. rise of hours between the 1970s and the 1990s, which was driven partly by a declining disutility of work and partly by compositional changes.

The 125-page paper is thorough and comprehensive, showing that U.S. welfare benefits, especially Medicaid, have suppressed employment:

… We observe that benefits to labor income have increased for most OECD countries in our sample. However, the increase is larger in the United States, especially after around 2000. … We observe a negative—and, in the second and third panels, statistically significant—relationship between benefits and hours worked. A 5 percentage points increase in benefits relative to labor income is associated with a roughly 2 percent decline in hours worked.

More benefits, fewer hours worked. The United States has erased its strong incentives for labor-force participation, strictly through government policy, the paper concludes:

Though in the 1990s Americans used to work much more than non-Americans, twenty years later, roughly half of this gap has disappeared. In this paper, we document trends in hours worked across countries and offer a comparative study on the convergence of hours worked. We develop a parsimonious model of labor supply and estimate it with detailed measurements from various micro-level and aggregate datasets. We use our model to run a horse race between various competing explanations and assess quantitatively the convergence of hours worked between non-U.S. countries and the United States after the 2000s. Our main finding is that U.S. hours per person declined after the 2000s because of the rise of benefits provided to the non-employed.

Among these benefits, we find the most important role for health benefits and, in particular, Medicaid. For non-U.S. countries, the rise of labor supply is generally accounted for by a rise of wages and falling fixed costs and disutility of work. The latter is also consistent with the rise of hours in the United States between the 1970s and the 1990s, which was driven by compositional changes and a declining disutility of work.

The conclusion is obvious: stop paying people so much not to produce.

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org