Life, Liberty, Property #141: Tremors in Private-Credit Market Confirm Fed’s Economic Damage

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

- Tremors in Private-Credit Market Confirm Fed’s Economic Damage

- Video of the Week: Record Pollen Levels Reveal Unexpected Climate Reality Check

- The Scariest Economic Danger from Oil Price Shocks

Tremors in Private-Credit Market Confirm Fed’s Economic Damage

Rising woes in the world of private credit are bringing new attention to investment risks. Attention to risk is always a good thing. It is too bad that the awareness generally intensifies only after excessive risk-taking has expanded deep into the pockets of smaller investors who did not have the ability to recognize how rickety their financial foundations were becoming.

One of the best examples of this phenomenon is the housing crash of the mid-2000s, which sparked the Great Recession. Forcefully encouraged by the federal government and the private financial institutions who relied on federal guarantees and other schemes to reduce their own risk, Americans borrowed heavily to buy houses with subprime mortgages, minimal down payments, and variable interest rates, “investing” more money in those properties than they were really worth.

It was a classic speculative bubble, and one that had its worst effects on ordinary people. Houses are not a liquid asset, and those who borrowed heavily to buy a house well above their means paid dearly as banks foreclosed on their loans.

What now appears to be a bubble in private credit is a similar case, argues the investment advisory website Fringe Finance (FF). In a highly informative article on Friday, FF notes a rising awareness of the current problem’s similarity to the subprime mortgage crisis:

First you had Apollo come out and literally say “all” marks across the entire industry were “wrong”. Then, bond king Jeff Gundlach drew direct parallels to the subprime mortgage market before the 2008 financial crisis and warning that the risks are widely misunderstood. Just days ago, Jamie Dimon also described, in his latest letter, how the area could become a serious problem.

FF extensively quotes and discusses the insights of investor and writer Howard Marks, whose memo to his Oaktree clients last Thursday warned, “the pressure is already manifesting in investor behavior. In the most recent quarter, investors withdrew nearly 8% from the flagship private credit fund of Blackstone Inc.,” as News Directory 3 (ND3) phrases it.

Though Marks told CNBC on March 5 that “There’s not a systemic problem with private credit,” he appears to have changed his thinking in the weeks since. Seeking Alpha reports:

In a memo to Oaktree clients Thursday, veteran investor Howard Marks outlined growing concerns about the private credit (VPC) market, particularly direct lending, as the sector faces its first major test since the 2008 Global Financial Crisis.

Marks traces the evolution of credit markets from the late 1970s through today, noting how direct lending exploded over the past 15 years as banks pulled back from risky lending. The sector has ballooned from roughly $150B two decades ago to about $2T in direct loans.

“I imagine some direct lending managers accepted too much money and invested it too fast, applying standards that were too low and setting the scene for a correction,” Marks wrote.

The veteran investor says that the brisk expansion of the sector has created risks of its own, ND3 notes:

This caution follows a period of rapid growth in the industry. On March 5, 2026, Marks stated on CNBC that direct lending had ballooned to a market exceeding $1 trillion from its early development around 2011.

While the growth has been substantial, Marks noted that the risk primarily stems from the pace of this expansion, which he suggests could expose lenders with weaker credit analysis when market conditions shift.

Marks argues that investors chasing big returns took greater risks than the fundamentals of the investments warranted, bringing on a correction, Seeking Alpha reports:

Marks points to recent bankruptcies at First Brands and Tricolor, which “caught credit investors by surprise” and raised concerns about possible fraud. Some investors in non-traded business development companies have faced redemption limits when attempting to withdraw their money. Meanwhile, investors sought to get back more than $20B of their investments from private credit firms in Q1 2026

That is a good description of a bubble. “And that’s exactly the point Howard Marks is making in his latest memo published April 9, 2026: the risks in private credit didn’t suddenly appear—they were always there,” FF writes. Marks explicitly describes the situation as a bubble, FF observes:

As Marks reminds readers, “Extreme upsurges in the popularity of novel forms of investment – those commonly labeled ‘bubbles’—invariably have certain features in common.” That framing is essential: he’s not saying private credit is uniquely flawed—he’s saying it’s behaving exactly like every hot financial trend before it.

Direct lending, the centerpiece of today’s private credit boom, followed that script almost perfectly. In its early days, it offered strong returns, tight protections, and attractive yields because there wasn’t enough capital chasing deals. Lenders had the upper hand. But success attracted attention—and attention attracted money.

That influx of capital is where Marks sees the turning point. As more firms entered the space and more money flooded in, competition increased. And when lenders compete, standards fall. Yields compress, protections weaken, and risk quietly builds beneath the surface.

In short, expanding demand pushed prices up and risk-aversion down.

I believe that the Federal Reserve’s tightening of the money supply and raising of interest rates since mid-2022 have forced a reckoning throughout the economy as dollars have become (slightly) scarcer (in comparison with GDP growth) and thus more valuable, meaning more precious than they were during the Obama years and pandemic era of near-zero interest rates:

“Marks referenced a common industry adage during his March 5, 2026, appearance on CNBC: ‘the worst of loans are made in the best of times,” ND3 reports. Private credit is getting corrected rather harshly because the relative newness of the sector and the distortions the Fed created through near-zero interest rates caused a paucity of knowledge about the real values of these investments. FF describes the situation as follows:

One of Marks’ most important points is that private credit hasn’t been properly stress-tested. Most of the industry was built after 2008, meaning it has largely operated in a benign environment—low rates, steady growth, and supportive markets. Many managers—and many investors—have never experienced what happens when conditions turn.

This creates a dangerous illusion. Private loans appear stable because they don’t trade frequently. Their prices don’t swing day to day like public bonds. But Marks emphasizes that this is not because they are less risky—it’s because the risk isn’t visible. As he puts it bluntly, “Direct loans embody no less credit risk than liquid credit instruments… It just isn’t reflected as readily in prices.” [Emphasis in original.]

In fact, that lack of transparency may have made things worse. Investors interpreted smooth returns as safety, which encouraged even more capital to flow in. This, in turn, accelerated the cycle: more money, more competition, weaker deals.

Marks suggests that the industry may have reached a point where too much capital was deployed too quickly and at too low a standard. Some managers, he implies, accepted more money than they could prudently invest, leading them to stretch on terms or borrower quality just to put capital to work.

FF’s description of the situation calls to mind the subprime crisis and the savings and loan debacle of the 1980s and early ’90s, with interest-rate increases putting heavy pressure on leveraged investments of unexpectedly imprecise value:

At the same time, liquidity issues have started to surface. Investors in certain private credit vehicles, particularly those marketed to individuals, have found that they can’t withdraw their money as easily as expected. Redemption limits, which seemed theoretical in good times, suddenly became very real.

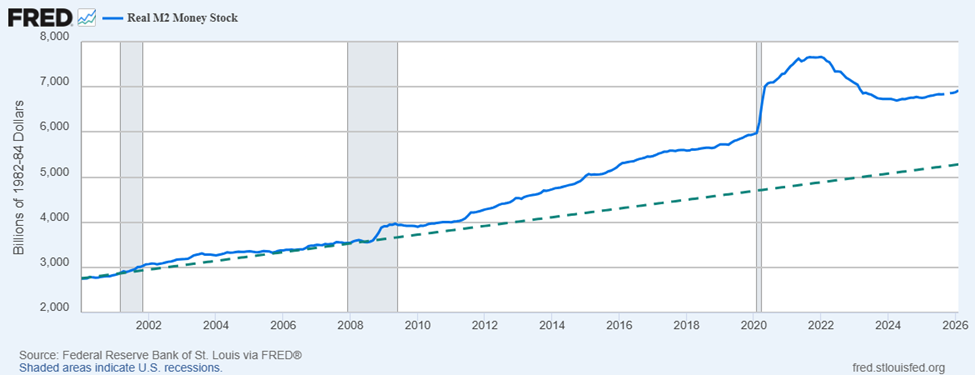

The pressure in the private-credit sector is a painful but beneficial process as a less-irresponsible treatment of the money supply diminishes the massive central-bank-imposed distortions of the nation’s financial system that have been torquing ever-further for nearly two decades, as the M2 chart above indicates. Years of easy money caused an enormous misallocation of resources all across the U.S. economy by falsifying price signals everywhere.

The nation’s economy has desperately needed a movement of prices of all things toward their real relative values. Though beneficial overall, the correction will cause a good deal of pain to those who were mistaken in their valuations of the enterprises in which they chose to invest. Too bad that the federal government and the Federal Reserve’s Open Market Committee will not pay that price themselves.

Sources: Fringe Finance; News Directory 3; Seeking Alpha

Video of the Week

Your car is covered in pollen, your eyes are itchy, and yes—allergy season is starting earlier and lasting longer. But here’s what the media won’t tell you: the same conditions making you sneeze are also driving unprecedented global greening, record crop yields, and thriving wildlife populations. 🌍

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Click here to get it at Amazon.

The Scariest Economic Danger from Oil Price Shocks

As the Iran War crimped oil supplies and drove prices radically higher, the effect on inflation has arisen as a major concern.

The conventional wisdom holds that oil price increases lead to inflation. The higher cost of inputs to economic production gets passed on to consumers and creates generalized inflation, the story goes. Writing at Mises Wire, however, economist and Mises Institute associated scholar Frank Shostak provides a highly astute examination of whether oil prices can cause inflation.

Taking the issue from a properly microeconomic (Austrian School) perspective, Shostak asks the right questions, beginning with who sets prices and how they do so:

[I]s it valid to suggest that the price of oil could be a key determinant of the prices of goods and services? Producers of goods and services set asking prices. It is also true that producers, while setting prices[,] take into account various production costs, including the cost of energy.

“Setting a price,” however, is not the same as getting a price, Shostak observes:

Whether the asking price offered by producers will be realized in the market place hinges on consumers’ acceptance or rejection of the asking price. Consumers dictate whether the price set by producers is “right.” …

If consumers don’t have the money or do not value the goods at the prices asked by producers, then the prices asked will not be realized.

Prices reveal the relative values of goods, services, savings, investments, commodities, and all sorts of resources by rising and falling as sellers and purchasers of those items reach agreements to trade them among one another. Those prices will be an accurate reflection of relative values, absent any major distortions imposed through force or fraud.

The price system thus results in a distribution of goods, services, commodities, savings, etc. that best approximates the most-valued uses of all those items.

A reliable currency helps ensure price signals are accurate, thus maximizing economic efficiency and hence overall prosperity. If the currency is holding a steady value, changes in some prices will cause the system to adjust accordingly. As Shostak writes,

In a monetary economy, prices are usually the amount of money exchanged for other goods and services. A price is the sum of money paid for a unit of a good. If the stock of money rises while all other things remain intact obviously this must lead to more money being spent on the unchanged stock of goods—an uneven increase in prices of goods.

If the price of oil goes up, and if people continue to use the same amount of oil as before, then this means that people would now be forced to allocate more money for oil. If people’s money stock remains unchanged, then this means that less money is available for other goods and services, all other things being equal.

The overall money spent on goods does not necessarily change, only the composition of spending has altered here, with more on oil and less on other goods. Hence, the prices of goods or money per unit of goods remains unchanged.

The changes in “the composition of spending” are a solution, not a problem: they reflect the changing values of things as supplies of goods and services fluctuate. If the nation does not alter the money stock significantly more or less than the overall change in the production of goods and services (including capital inputs), no changes in the supplies of goods, services, commodities, and the like can cause a generalized inflation. Shostak writes,

From this we can infer that the rate of increase in the prices of goods and services in general will be constrained by the growth rate of money supply, all other things being equal, and not by the growth rate of the price of oil. It is not possible for increases in the price of oil to set in motion a general increase in the prices of goods and services without corresponding support from money supply. Furthermore, the reliance on correlations to establish causality is likely to produce misleading results. All that correlation does is to describe, it doesn’t explain.

What people often perceive as inflation is this ongoing process of price changes suddenly affecting particularly desired goods and services. Concerns about changes in the Consumer Price Index often reflect this misunderstanding, notes Research Fellow Kristian Fors of The Independent Institute:

Many people often confuse inflation with the consumer price index (CPI), which is a basket of goods designed to measure changes in the price of consumer goods and services. Changes in the CPI do not constitute inflation; rather, the CPI and its many variants are attempts to measure inflation. In other words, the CPI can be affected by variables unrelated to the monetary phenomenon of inflation, such as the avian flu.

Fors quotes the oft-cited observation by Nobel Prize-winning economist Milton Friedman that central banks are responsible for inflation:

Milton Friedman once famously stated that “inflation always and everywhere is a monetary phenomenon.” Inflation results from an increase in the money supply and a decline in the real value of fiat currency relative to goods and services. Prices can increase for a variety of reasons unrelated to the money supply, but that is not inflation.

Inflation is not an organic phenomenon stemming from supply and demand, but rather a policy decision determined directly by central banks. Implying that central banks monitor and respond to inflation distorts the reality that they are the ones who cause it.

The real cause of any inflation that arises after an oil-price shock is the central bank’s response to the natural economic effects of the change in petroleum prices:

- An increase in the cost of oil raises the costs of producing goods and services, pushing down economic growth.

- The central bank responds by loosening the money supply to stimulate growth (often after having tightened the money supply in a forlorn attempt to push down oil prices, which strangled economic growth further).

- The money supply increase in a time of suppressed economic growth causes real, generalized inflation.

As always, the best response of the government and central bank to a crisis is to do nothing.

Sources: Mises Wire; The Independent Institute

Important Heartland Policy Study

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute

1933 North Meacham Road, Suite 559

Schaumburg, IL 60173

p: 312/377-4000

f: 312/277-4122

e: [email protected]

Website: Heartland.org