A few months after the passage of President Obama’s health care overhaul, a postcard arrived which led me to believe there may be a benefit coming to my small firm. The mailing from the Treasury Department touted a generous 35 percent tax credit to firms with less than 25 full-time employees averaging less than $50,000 per year in wages, a category which includes my company.

In fact, I thought we were right in the sweet spot, with 17 full-time employees averaging slightly more than $42,000 per year.

Small Business Needs Relief

I manage Pinney Printing Company in Sterling, Illinois. I’m the president of the firm, which our family has owned for 100 years. Health care expenses are a major obstacle to Pinney’s long-term prosperity. Each year in May, our policy renews and we are faced with double-digit premium increases—20-40 percent in recent years.

Some of the increase is absorbed by the company, and some gets passed some on to the employees through higher premiums, deductibles, and copays. We have experimented with self-funding and high-deductible health plans. Last year we were forced to downgrade to an HMO plan.

We are nearing the end of our rope, so I was hopeful to learn there could be some benefit for us in the new law.

Postcard in hand, I did a quick calculation and figured our tax credit should be about $28,000. That is 35 percent of the $80,000 we expect to spend this year on employee health care premiums. I phoned our health insurance broker and inquired whether anything special had to be done, not wanting to be excluded by some technicality. He reported there was no special requirements—more good news.

Barrier to Tax Credit

But there was a problem. A few weeks later I received an email with a link to the National Federation of Independent Business’s online calculator, designed to help firms determine their qualifications for the tax credit. I plugged in our numbers, and pressed “update” to yield a calculation of . . . zero—zip, nada!

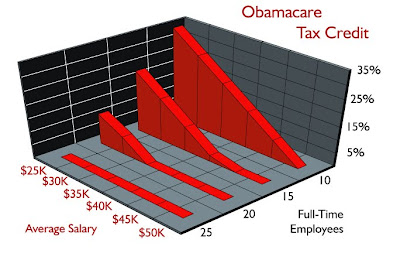

Double-checking, I tried again and again, finally concluding the 35 percent tax credit will be available only to firms with ten or fewer employees averaging $25,000 or less per year. Increasing either factor—number of employees or average salary— greatly diminishes the magnitude of the tax credit. Increasing both factors yields a parabolic reduction in the result.

Being in the graphic arts industry, I decided to create a chart diagramming the limits of this “generous” tax break:

Not one to give up easily, I continued my pursuit. Surely there was some benefit in this for me, after years and years of paying the toll for big-government programs and receiving nothing.

The vague language on the postcard instructed readers to learn more at www.irs.gov. There it said to exclude owners, those having a stake of 5 percent or more, from all of the input values. I eagerly entered new numbers—subtracting myself, my annual premium, and my salary. This brought our headcount down to 16 and dropped the average salary to $40,000.

I entered the numbers, and the NFIB calculator displayed the same result—another big goose egg.

Inviting Employee Layoffs

Talk about unintended consequences! My firm would have to reduce its workforce and cut employee wages to benefit from the newly enacted Patient Protection and Affordable Care Act. Is this what the objective should be?

I would never consider taking such action. Most of the employees have worked at Pinney for twenty years or more. It did get me thinking, though: Maybe we could divide Pinney Printing Company into two smaller firms. While I’m no expert at gaming the government, like some people, it’s certainly a possibility many will consider.

I feel foolish now, after getting my hopes up for a government solution to our problem. Our firm is running out of affordable options.

It is my belief that health insurance should be decoupled from employment and bought by individuals and families in the same way automobile insurance is purchased. It is my fear that Obamacare is a step in the wrong direction and matters will get worse, not better, for Pinney Printing Company and others like us.

Charles Arp ([email protected]) writes from Sterling, Illinois.

Internet Resources

NFIB Credit Calculator: http://www.nfib.com/issues-elections/healthcare/credit-calculator