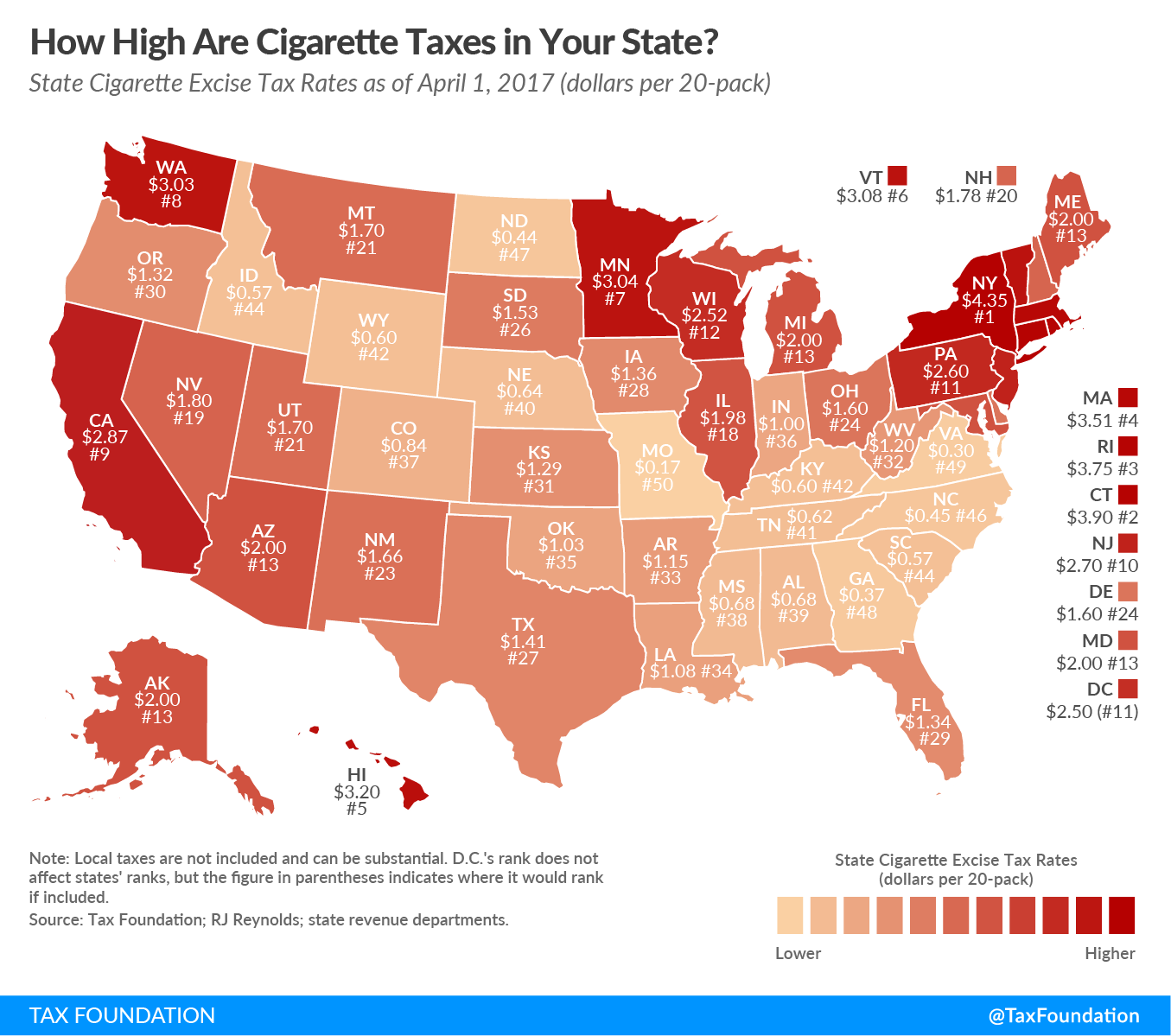

Voters in South Dakota may soon be considering a new proposal to dramatically increase the state’s tobacco tax. The current cigarette tax is levied at a rate of 76.5 mills per cigarette, making the average tax on a 20-cigarette pack $1.53. The tax on other tobacco products is set at 35 percent of the wholesale price of the product.

According to the Tax Foundation, South Dakota’s cigarette tax rate is now slightly lower than the national average ($1.68 per pack), but it’s higher than four of its six bordering states. The proposed ballot measure would give South Dakota voters three options, two of which are rate increases and the third a rejection of a rate increase. The two rate-hike options would increase the cigarettes by either 101.5 mills per cigarette, raising the tax to $2.03 per pack, or 126.5 mills per cigarette, increasing the tax by a dollar, to $2.53 per pack.

Under the proposed increases, the tax on other tobacco products would be increased to either 45 percent or 55 percent. According to the Argus Leader, the projected revenue from the tax would go to the general fund, tobacco prevention programs, and technical school funding.

South Dakota’s tobacco tax rates now rank 26th in the country. According to the Tax Foundation, the two rates under consideration would give the state either the 13th or 17th highest rate and would move the state’s rate past Montana’s tax rate. Only Minnesota would have a higher rate in the region.

Although reducing smoking rates may be a noble goal, raising tobacco taxes rarely works as intended and frequently has many negative effects. Sin taxes have a strong detrimental effect on local small businesses; when they are implemented, retailers and wholesalers find themselves with decreased sales, as consumers seek to avoid the tax by purchasing products outside the county, city, or state imposing the tax.

Tobacco taxes are an unreliable and shrinking tax-revenue stream, relying on this tax for any major expenditure will likely create budget problems in the future. While sin taxes do sometimes result in increased revenue over the short term, they often lead to an even greater increase in expenditures, which often cannot be supported by the tax over the long term, thereby creating budget shortfalls.

According to the data from the U.S. Census Bureau, state revenue from tobacco product taxes fell in 2013 by 0.9 percent, to $17 billion. That decrease followed a 0.5 percent reduction in 2012. The National Taxpayers Union Foundation has found tobacco tax collections failed to meet initial revenue targets in 72 out of 101 recent tax increases. The Tax Foundation reported similar results after South Dakota’s last hike, after an initial increase, revenue collection began to decrease.

The tax hike proposal is also likely to drive consumers to purchase tobacco in other states and increase black-market sales of tobacco products. The Tax Foundation notes South Dakota already has the 17th-highest proportion of smuggled cigarettes, and Smuggling is likely to increase even more if South Dakota were to increase tobacco taxes further, making tax revenue less stable.

Cigarette taxes are also highly regressive, unduly burdening moderate- and low-income individuals. According to the Bureau of Labor Statistics, 95.8 percent of tobacco expenditures are made by consumer units (people spending together) who earn less than $150,000 a year.

Increasing taxes on tobacco products would reduce South Dakota’s economic competitiveness and encourage unsustainable increases in government spending, all while placing an excessive burden on lower-income taxpayers. Instead of creating and increasing taxes, South Dakota should focus on spending and ways to make government more efficient.

The following documents provide additional information on tobacco taxes and other “sin” taxes.

South Dakota Lights Up Revenue Uncertainty with Proposed Tobacco Tax Hike

https://taxfoundation.org/south-dakota-lights-revenue-uncertainty-proposed-tobacco-tax-hike/

Raymond Roesler of the Tax Foundation examines two ballot proposals for South Dakota voters that would raise the state’s tax on cigarettes and other tobacco products. Proponents of the proposals say the taxes would raise additional revenue for the general fund, tobacco prevention programs, and technical school funding.

Cigarette Taxes and Cigarette Smuggling by State, 2014

https://taxfoundation.org/cigarette-taxes-and-cigarette-smuggling-state-2014/

Scott Drenkard and Joseph Henchman of the Tax Foundation examine tobacco taxes and their effect on cigarette smuggling across the United States. “One consequence of high state cigarette tax rates has been increased smuggling as people procure discounted packs from low-tax states to sell in high-tax states,” Drenkard and Henchman wrote. “Growing cigarette tax differentials have made cigarette smuggling both a national problem and in some cases, a lucrative criminal enterprise.”

Cigarette Taxes and Smoking

https://heartland.org/publications-resources/publications/cigarette-taxes-and-smoking

In this study from the Cato Institute, Kevin Callison and Robert Kaestner suggest future cigarette-tax increases will offer relatively few public health benefits, and they say the justification given for future taxes should be based on the public finance aspects of cigarette taxes, such as the regressiveness, volatility, or the rate of revenue growth associated with those taxes.

Ten Principles of State Fiscal Policy

https://heartland.org/publications-resources/publications/ten-principles-of-state-fiscal-policy

This Heartland Institute booklet provides policymakers and civic and business leaders a highly condensed yet easy-to-read guide to state fiscal policy matters. It presents the 10 most important principles of sound fiscal policy, from “Above all else: Keep taxes low,” to “Protect state employees from politics.”

Sin Taxes: Size, Growth, and Creation of the Sindustry

https://heartland.org/publications-resources/publications/sin-taxes-size-growth-and-creation-of-the-sindustry

Adam Hoffer of the Mercatus Center explores three criticisms of sin taxes. First, although advocates of sin taxes claim those taxes are justified because the “sinners” impose costs on society, taxing “sins” for general budget revenue contradicts that argument. Second, the economic burden of sin taxes falls disproportionately on low-income households. Third, the expanding number of goods being targeted results in unproductive lobbying aimed at preventing new industries from being considered “sinful.”

Five Things to Consider Before Raising Tobacco Taxes: A Review of the Research

https://heartland.org/news-opinion/news/five-things-to-consider-before-raising-tobacco-taxes-a-review-of-the-research

This Heartland Institute Policy Brief argues, “Tax increases above current levels are not justified by appealing to the costs smokers impose on nonsmokers. Smokers already pay more than this measure could justify.”

Debunking the “Tax Thee, But Not Me” Myth: Five Reasons Why Non-Smokers Should Oppose High Tobacco Taxes

http://www.ntu.org/main/press_issuebriefs.php?PressID=1001&org_name=NTU

The nonpartisan National Taxpayers Union observes, “The per-capita state and local tax burden in high-tobacco tax states is 8 percent above the national average, while the general tax bill for residents of low-tobacco tax states is 15 percent below the national average.”

Research & Commentary: Top Ten Reasons Not to Raise Tobacco Taxes

https://heartland.org/publications-resources/publications/research–commentary-top-ten-reasons-not-to-raise-tobacco-taxes

John Nothdurft of The Heartland Institute argues targeted tax increases serve only to push sound fiscal policies and real budget reforms to the public policy backburner. Legislators concerned about the public health effects of tobacco should encourage the use of readily available smoking cessation products and services instead of supporting bad tax policy.

Nothing in this Research & Commentary is intended to influence the passage of legislation, and it does not necessarily represent the views of The Heartland Institute. For further information on this and other topics, visit the Budget & Tax News website, The Heartland Institute’s website, and PolicyBot, Heartland’s free online research database.

The Heartland Institute can send an expert to your state to testify or brief your caucus; host an event in your state, or send you further information on a topic. Please don’t hesitate to contact us if we can be of assistance! If you have any questions or comments, contact John Nothdurft, Heartland’s director of government relations, at [email protected] or 312/377-4000.

Matthew Glans joined the staff of The Heartland Institute in November 2007 as legislative specialist for insurance and finance.

{kind=link}