Life, Liberty, Property #144: Debt-to-GDP Ratio Tops 100 Percent

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

- Debt-to-GDP Ratio Tops 100 Percent

- Video of the Week: Raids, Charges, and Indictments — In the Tank Podcast #534

- Oil Price Shocks and Inflation

- Justice Department Sues New Jersey over College Tuition Benefit for Illegal Immigration

Debt-to-GDP Ratio Tops 100 Percent

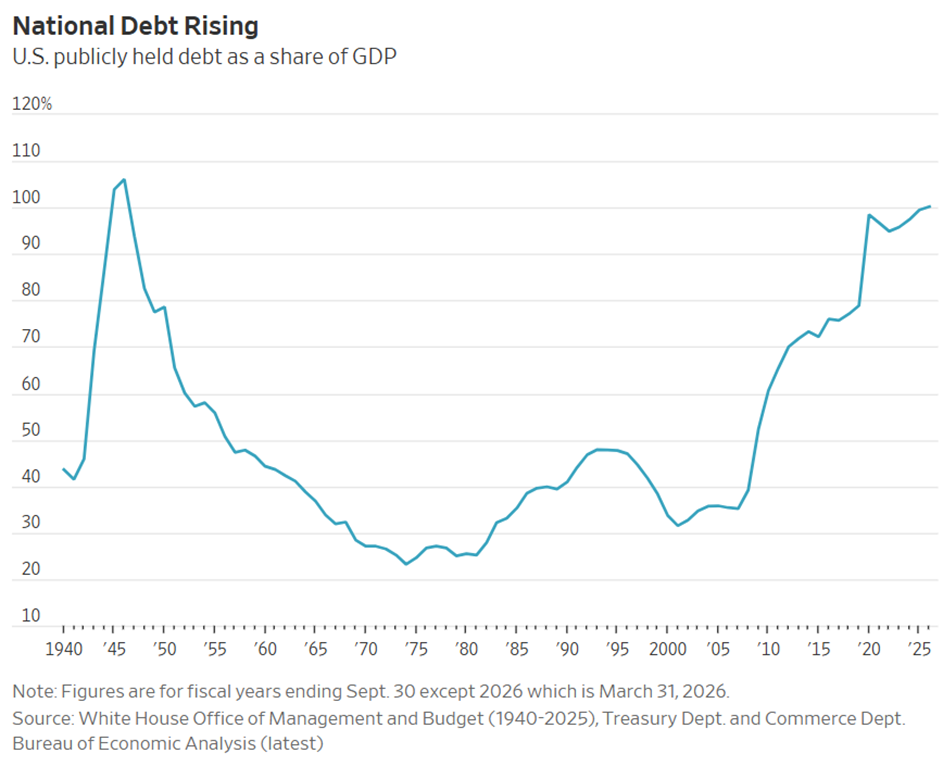

The federal debt crossed an ominous threshold last week, rising over 100 percent of national gross domestic product, tax policy reporter Richard Rubin notes in The Wall Street Journal:

As of March 31, the country’s publicly held debt was $31.265 trillion, while GDP over the preceding year was $31.216 trillion, according to data released Thursday. That puts the ratio at 100.2%, compared with 99.5% when the last fiscal year ended Sept. 30.

Here is the Journal’s chart illustrating the grim news:

Source: The Wall Street Journal

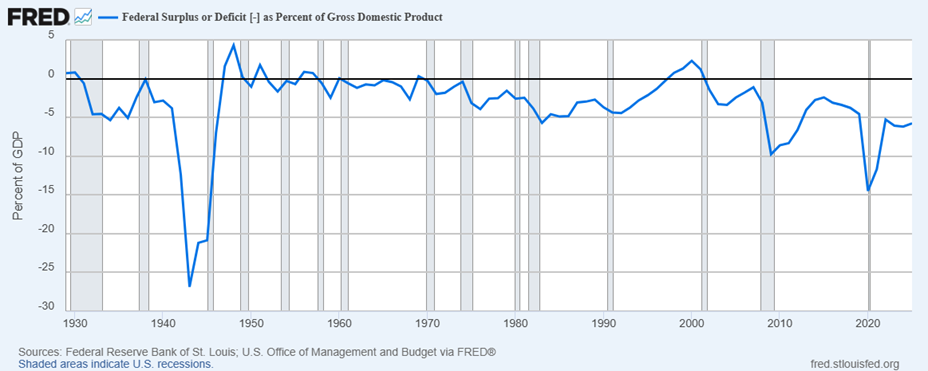

As the chart indicates, the debt-to-GDP rise accelerated during World War II, the Reagan and George H. W. Bush administrations, the Obama administration, and the pandemic. Although the pace of increase has slowed since 2020, the overall ratio remains near the world war level. The federal deficit-to-GDP ratio is higher than at any time since the Great Recession and exceeded only by the WWII years:

Source: Federal Reserve Bank of St. Louis

The trend is for ever-higher debt as a percent of GDP, Rubin notes:

As of March 31, the country’s publicly held debt was $31.265 trillion, while GDP over the preceding year was $31.216 trillion, according to data released Thursday. That puts the ratio at 100.2%, compared with 99.5% when the last fiscal year ended Sept. 30. That figure will likely climb for the foreseeable future because the federal government is running historically large annual deficits of nearly 6% of GDP, which add to the debt.

The government is spending $1.33 for every dollar it collects in revenue, and the budget deficit this year is projected at $1.9 trillion. That is little changed from 2025 as Republicans’ tax cuts kick in before their spending cuts take effect. The final tally will depend on Iran war spending, tariff refunds and the strength of the economy.

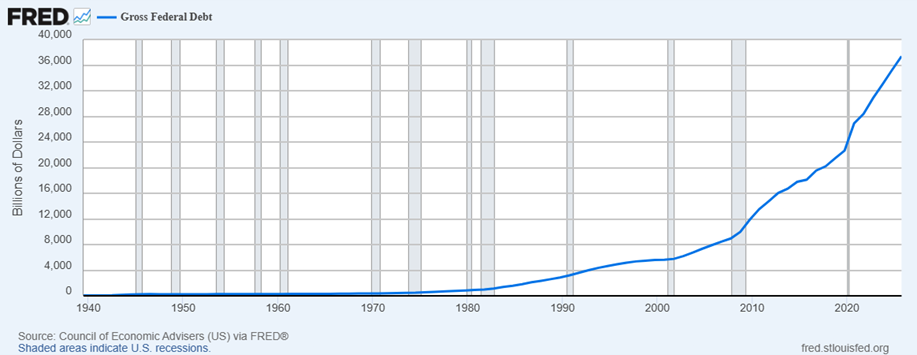

Federal debt reaching 100 percent of GDP does not have any specific effect on the economy in itself. It is just an indicator of how far federal government spending has risen above the amount the government can persuade the American people to pay for through taxes. Here is what that difference looks like:

Source: Federal Reserve Bank of St. Louis

The first members of the Silent Generation became eligible to vote in U.S. elections in 1949. The Baby Boom generation started in in 1946 and became eligible to vote in national elections in 1967. Generation X began to reach voting age in 1983, the Millennial Generation in 1999, and the Zoomers in 2015.

Make of that what you will. The important point is that the federal government’ deficit spending diminishes economic expansion, which pushes GDP below its potential, and that exacerbates the situation. It’s a classic debt spiral. Rubin describes the current situation as follows:

The debt-to-GDP ratio is economists’ preferred metric for how much the country’s borrowing weighs on the economy. As it rises, debt consumes resources that could be used more productively elsewhere.

The government also becomes more sensitive to interest rates as debt grows. One in seven dollars of federal spending now goes to interest. A 0.1 percentage-point interest-rate increase would cost $379 billion over 10 years, according to the Congressional Budget Office.

Without changes, the U.S. is headed toward debt ratios already reached in France, Italy, Greece and Japan, which have faced varying degrees of economic stress as a result. That said, the U.S. has more room to borrow than those countries because it controls the world’s reserve currency, and because of Treasury debt’s position as a haven for investors.

The dollar’s status as reserve currency is based in part on a deal the U.S. government made with Saudia Arabia in 1974 to require buyers of its oil to pay in U.S. dollars. The rise of the petrodollar greatly increased demand for the U.S. dollar, making the greenback the most reliable big currency in the world.

Perhaps even more important to the dollar’s status as reserve currency is the inherent strength of the U.S. economy based on our nation’s historical commitment to free markets. The federal government has sapped that strength badly over the decades, through wildly excessive spending, unnecessary and unconstitutional regulation, other economic distortions, and a general transfer of resources and economic choice away from the people and into the government bureaucracy.

As the charts above indicate, the U.S. government has spent the years since 1974 borrowing enormous amounts of money for itself to spend on vote-buying with income-transfer payments. This has eroded the value of the U.S. dollar through continual inflation, which reached a crisis during 2021 through 2023 as inflation heated up after the pandemic. Economic growth has slowed.

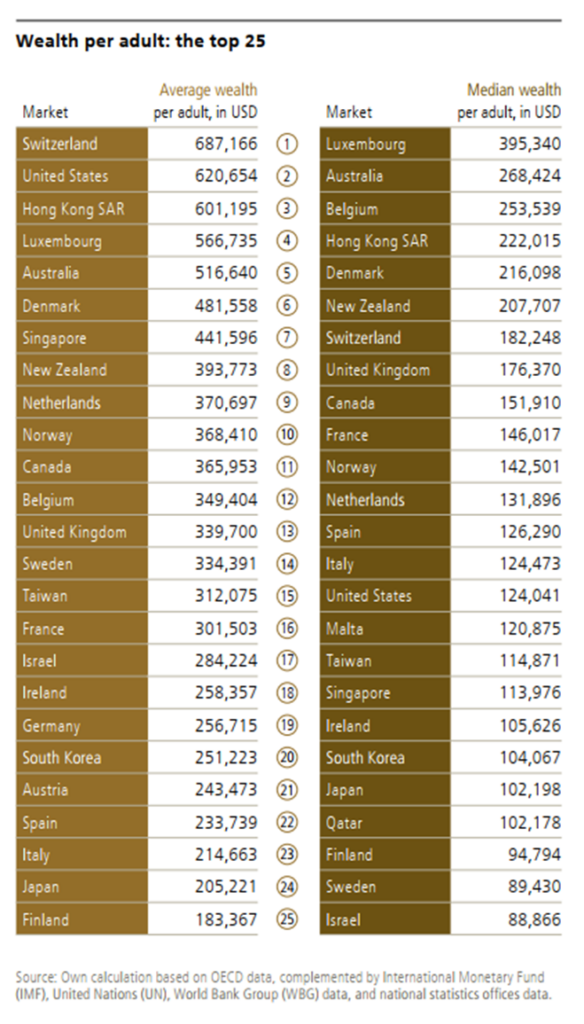

It is true that the debt-to-GDP ratio is not some sort of magic number. GDP measures economic activity, not wealth. The United States remains the world’s wealthiest nation by far, and wealth is the real measure of tolerance for debt:

Source: Global Wealth Report 2025, UBS Global Wealth Management

As economist John Rutledge notes, “no matter what is in the headlines or the economic reports, the future of our economy will be determined by the stability of our enormous balance sheet.” The United States is very far from running out of wealth, Rutledge argues:

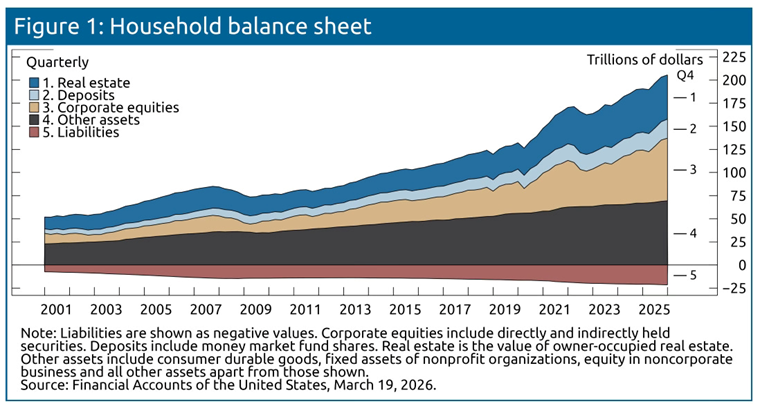

The Q4/25 report on our big balance sheet, released late last week to a wall of silence from the Fed, the economics community, and the financial press, is more important for investors to understand than the employment report, the CPI report, or the FOMC minutes. On 12/31/25 total U.S. assets were valued at $618 trillion. That’s 19.7 year’s U.S. GDP ($31.4 trillion). U.S. households and businesses chose to hold $195 trillion (32%) of that in the form of tangible assets, like homes, used cars, and gold coins and $423 trillion (68%) as financial assets, like stocks, bonds, and money market funds.

Chart 1: Household Balance Sheet. p. 1

Household net worth equals $184 trillion, which is worth 7.9 years of disposable income. Households own $206 trillion of assets, including $52 trillion of homes, of which 71% ($34 trillion) is net owners equity. They have just $21 trillion of total liabilities, almost all of which is home mortgages. Net worth has grown by about 7% per year for the last 50 years.

The U.S. government debt amounts to 5 percent of the nation’s total assets. Although that is far, far more than is either advisable or justifiable, it is a little less than half the average household’s debt, which is 10.2 percent according to Rutledge’s numbers.

Wealth is natural resources plus human ingenuity. The United States has an abundance of both, Rutledge notes:

I want you to see how big these numbers are compared with the usual numbers people worry about in the financial press and compared with anything in the national income accounts. And wouldn’t it be shocking if that were not true. The balance sheet is a huge pile of stuff, basically equal to everything we received for free from Mother Nature, plus everything that everybody who has ever lived here has produced that didn’t wear out yet. (Think Ben Franklin and the Liberty Bell.) Plus whatever we have produced in our own lifetimes (142 million homes, 285 million used cars, and the sofa in your living room) that we haven’t worn out yet.

The American people have always found a way to stay ahead of the destructive power of government, Rutledge notes:

Why does this matter? Because it will help you sleep better at night. Whatever your politics, it is clear that there are some big messes in the world that we have to clean up. But the sheer size and duration of our stock of assets should give us a lot of comfort that no single group of policy makers from either party can destroy the engine that powers the U.S. economy. So, although I keep my eyes open for the credit crises2 we get whacked with once every decade or so, I have faith that this economy will hold together and keep growing for a long, long time.

Rutledge believes that we are “about due” for a credit crisis, but we always get through them as people readjust their priorities to realign with reality. The real crisis that lies ahead is not bankruptcy of the American people but a bankrupt federal government.

That is good news. If the federal government loses its ability to borrow money ever-more furiously as the massive sovereign debt pushes up interest rates, the collapse of the government’s borrowing ability will create a massive disruption in the economy and society in general. The American people, however, can and will survive and thrive, probably with a much-smaller government on the other side of the commotion. That last part sounds beautiful.

We can avert even that form of crisis by cutting spending and regulation. We will not do so, however, because members of Congress cannot bear the idea of being held responsible for tens of millions of Americans’ loss of freebies paid for by other taxpayers. No amount of dire warnings and symbolic thresholds will change that.

Sources: The Wall Street Journal; Asset-First Economics

Video of the Week

Federal agents raided more than 20 businesses this week in Minneapolis as the fight against fraud continues, and Governor Tim Walz is trying to take credit, but the public isn’t falling for it. Another scam was busted at the Supreme Court, which issued a decision on race-based gerrymandering in Louisiana, stating definitively that the practice is unconstitutional.

An advisor to Anthony Fauci has been charged with conspiracy against the United States; destruction, alteration, or falsification of records in federal investigations; concealment, removal, or mutilation of records; and aiding and abetting, at the same time, former FBI director James Comey has been indicted over his threatening social media posts against President Trump. After yet another assassination attempt on the President, these issues are taken very seriously by the DOJ.

On UNHINGED: Ann Arbor Michigan is removing neighborhood watch signs to make neighborhoods feel more “inclusive.” Not a joke. The Heartland Institute’s Linnea Lueken, Jim Lakely, Chris Talgo, and S.T. Karnick will talk about all of this and more on Episode #534 of the In The Tank Podcast.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Click here to get it at Amazon.

Oil Price Shocks and Inflation

Like tariffs, “excessive demand,” solar eclipses, and witches’ curses, oil price hikes cannot cause inflation. Only foolish reactions by governments and central banks can do that, as I noted early last month in regard to concerns that the oil price shocks from the Iran conflict and blockade would cause inflation in the United States. That is a point I’ve made regularly in Life, Liberty, Property, going all the way back to the very first issue in December 2022. (Not available online at present. I’ll have to remedy that.)

Self-proclaimed “Grumpy Economist” John H. Cochrane of the Hoover Institution explains this very well in an article published last Friday on his Substack of that name, reprinted from The Wall Street Journal. His thesis is simple and straightforward:

… energy prices turn into recessions only if bad policies compound their effects. Price controls, credit controls, windfall profits taxes, export controls, the 55-mph speed limit, corn ethanol, cardigan sweaters, malaise, and a slow-to-react Federal Reserve all fed the misery of the 1970s. They need not do so again.

This is the most important thing to keep in mind in regard to the Iran oil price shock: everything will move back into line and people will allocate their investments and purchases to their own liking and best preferences if the government and central leave it to us to do so. As I wrote in LLP issue 141 (“The Scariest Economic Danger from Oil Price Shocks”), “If the nation does not alter the money stock significantly more or less than the overall change in the production of goods and services (including capital inputs), no changes in the supplies of goods, services, commodities, and the like can cause a generalized inflation.”

Governments’ attempts to mollify potential voters (and donors) disturbed by temporary price increases worsen the price shocks and prolong the economic destruction. Cochrane explains:

Higher gasoline prices need not mean inflation. But governments will produce inflation if they hand out money so people can pay higher prices. Price controls mean gas lines, which increase economic damage. The most productive users who can’t substitute away then can’t get the energy they need, and suppliers see no incentive to help. Windfall profits taxes in bad times dampen the incentive to invest in spare capacity in good times. The first principle of economics is: Don’t transfer income by distorting prices. The first principle of politics is the opposite.

The last two sentences of that paragraph are critical to an understanding of how and why governments and central banks suppress economic growth when trying to restore recent economic conditions whenever things change. That is in fact codified in federal law, in the “dual mandate” Congress has set for the Federal Reserve (Fed). Here is how the Fed phrases it:

The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”1 Even though the act lists three distinct goals of monetary policy, the Fed’s mandate for monetary policy is commonly known as the dual mandate. The reason is that an economy in which people who want to work either have a job or are likely to find one fairly quickly and in which the price level (meaning a broad measure of the price of goods and services purchased by consumers) is stable creates the conditions needed for interest rates to settle at moderate levels.

The natural processes of macroeconomic adjustment that occur in reaction to price shocks caused by changes in the supplies of critical goods and services are the cumulative result of the incalculable number of decisions made by the entire population. Governments intrude in these choices because they consider the results to be to their political disadvantage. Central banks serve those governments, as the Fed’s dual mandate indicates.

In addition to the direct damage these government interventions do, the unhappy results compound as the government reacts to the new situation it has created, which is by nature not optimal, as explained above. Cochrane writes,

High energy prices do slow the economy. But a slowdown turns into a recession only when something financial goes wrong. The aftermath of an energy price spike depends a lot on how central banks respond. If the Fed reacts slowly, along with harmful economic policies, stagflation could again break out quickly, and then recession could follow when the Fed reacts to inflation.

The central bank will be tempted to react to supply-induced softening with demand stimulus. It will be tempted to “look through,” i.e., ignore, the transitory inflation of an oil-price shock as it looked through Covid-era inflation, until inflation reached 8%. Fed officials planned to look through tariffs as well.

But, as in 1979, people who saw substantial inflation may be quick to expect more inflation, and then the Fed will have to react strongly, as it did in 1980. I also fear that the Fed may be paralyzed during its change of leadership or may try to avoid moving interest rates by relying on quantitative tightening or credit restrictions. All that will cause needless financial turmoil.

Cochrane’s conclusion is that the government should do nothing when such crises arise:

What should government do about rising energy prices? Nothing. Or, more concretely, get out of the way, ease restrictions, and let the market work its magic of sending energy to the most economically important uses while encouraging others to save, substitute or provide new energy. Keep inflation under control, and don’t induce financial problems.

Cochrane’s recommendation is in line with my own: maintain stability of the currency, cut taxes, and reduce regulation.

Source: The Grumpy Economist

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Justice Department Sues New Jersey Over College Tuition Benefit for Illegal Immigration

The U.S. government filed a complaint in federal court last week to disallow the state of New Jersey from giving in-state tuition rates and financial aid to residents who are in the country illegally. Those policies violate federal law, the complaint notes, correctly.

After 30 years of ignoring the law, the federal government has decided to begin enforcing it, The Epoch Times reports:

Assistant Attorney General Brett A. Shumate of the Justice Department’s Civil Division said this is a simple matter of federal law.

“In New Jersey and nationwide, colleges cannot provide benefits to illegal aliens that they do not provide to U.S. citizens,” he said. “This Department of Justice will not tolerate American students being treated like second-class citizens in their own country.”

The benefit is significant: out-of-state tuition rates are commonly more than double the cost of in-state tuition.

Under federal law, a state cannot provide a benefit to people residing in the country illegally if it does not offer that same benefit to U.S. citizens. The law obviously means all U.S. citizens, as the text of the statute does not place any limit on that term. That means a state may charge much-lower in-state tuition to people illegally residing in the United States only if it charges all U.S. citizens or legal residents in-state tuition as well.

Section 505 of Public Law 104-428 (see page 673), enacted in 1996, states the following:

Notwithstanding any other provision of law, an alien who is not lawfully present in the United States shall not be eligible on the basis of residence within a State (or a political subdivision) for any postsecondary education benefit unless a citizen or national of the United States is eligible for such a benefit (in no less an amount, duration, and scope) without regard to whether the citizen or national is such a resident.

The law requires the states to document the legal status of every immigrant receiving these benefits:

[T]he institution shall transmit to the Immigration and Naturalization Service either photostatic or other similar copies of such documents, or information from such documents, as specified by the Immigration and Naturalization Service, for official verification[.]

In 2021, 16 states and the District of Columbia had laws allowing aliens in the country illegally to pay in-state tuition rates, while charging out-of-state students higher, out-of-state tuition, and another seven state university systems allowed the practice as well, The Daily Signal reported last year.

The Justice Department (DOJ) began to file lawsuits to enforce the immigration status requirement in June of last year, starting with Texas. The state government immediately settled the case and signed a consent decree.

Since then, the DOJ has filed suits against several other states. Cases in Kentucky and Oklahoma “have led to orders declaring unconstitutional similar laws offering reduced tuition to illegal aliens,” and similar suits are pending in California, Illinois, and Virginia, The Epoch Times reports. In Minnesota, a district court judge dismissed the federal government’s lawsuit on March 27, arguing that U.S. citizens of other states could get in-state tuition rates if they jumped through a few extremely small hoops:

As Defendants point out, there are multiple ways a student could qualify for Resident Tuition without residing in Minnesota, such as attending a Minnesota high school while living in a neighboring state, or by attending a Minnesota boarding school. Whether the number of those students is large or small is irrelevant—unless the availability of the benefit provided by the State depends on residency, there is no but-for causation.

The judge dismissed the case with prejudice, meaning it cannot be refiled. For such cases, the federal government generally has 60 days to file an appeal, which would give the DOJ until the last week of this month to file. The judge’s reasoning invites an appeal. It is clearly wrong to argue that “[w]hether the number of those students is large or small is irrelevant”: the federal statute specifies “U.S. citizens” with no limits or qualifiers.

The federal government’s complaint in the New Jersey suit notes the state provides tuition and financial assistance to aliens in the country illegally, and it requests that the court order the state to enforce its laws and bring them into compliance with federal law, The Epoch Times story reports:

The complaint is aimed at New Jersey laws requiring colleges and universities to provide in-state tuition rates to all aliens who have residency in the state, regardless of whether they are lawfully present in the United States. It also attempts to bar state provisions for financial assistance and scholarships to illegal aliens.

States could easily comply with the federal law by denying in-state tuition to people who are residing in the United States illegally. Those so denied could either pay out-of-state tuition or comply with the nation’s immigration laws. These states have been favoring immigrant lawbreakers over legal residents of the United States. That is both illegal and unfair to their fellow Americans.

Sources: The Epoch Times; United States Government Publishing Office

Contact Us

The Heartland Institute

1933 North Meacham Road, Suite 559

Schaumburg, IL 60173

p: 312/377-4000

f: 312/277-4122

e: [email protected]

Website: Heartland.org