Life, Liberty, Property #145: U.S. Economy Is ‘Bad’ or ‘Terrible,’ Under-30s Say

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

U.S. Economy Is ‘Bad’ or ‘Terrible,’ Under-30s Say

Video of the Week: Innovation or Dystopia — In the Tank Podcast #535

Who Caused the Affordability Crisis?

Hot off the Presses!

‘Today’s crisis is a product of government errors, not greedy landlords, institutional investors, and so-called market failure.’

U.S. Economy Is ‘Bad’ or ‘Terrible,’ Under-30s Say

Young adults across the United States overwhelmingly say that the U.S. economy is currently “bad” or “terrible,” and “we’re seeing the consequences all over America.”

The illustration for Snyder’s article vividly conveys widespread despair and a sense that economic conditions are falling far short of young people’s expectations:

The well-documented rise in housing unaffordability, which I have covered regularly in this newsletter and examine the causes of which in my Heartland paper, has been a boon to older homeowners while concentrating its worst effects on those under the age of 40. Snyder writes,

Our young adults are being hit particularly hard. If you purchased a home 20 or 30 years ago, you are insulated from what is really going on out there. Housing costs are more unaffordable than ever, and many young people have completely given up on the dream of homeownership. Meanwhile, the employment market has gotten very tight, and this is especially true for entry-level jobs.

Do you know anyone under the age of 40 that is doing really well in this economy?

Yes, there are some exceptions, but in general our young adults are really struggling.

Young American adults are rebelling against those they hold responsible for their disappointment, Snyder writes:

It is undeniable that most of our young adults hate this economy.

In fact, a new survey that was just released found that a whopping 84 percent of Americans between the ages of 18 and 24 believe that economic conditions in the U.S. are either “bad” or “terrible”…

A recent survey by Generation Lab found that more than 8 in 10 young adults rate economic conditions in the U.S. as either bad or terrible.

The survey, conducted April 26-29, found that 55 percent of 546 respondents ages 18-24 said they view the economy as bad, while 29 percent said it was terrible.

The same survey discovered that 81 percent of Americans between the ages of 25 and 29 believe that economic conditions in the U.S. are either “bad” or “terrible”…

As for those in the 25-29 age range, 52 percent of 266 such respondents said the economy was bad. About 3 in 10 respondents said it was terrible, for a combined percentage of 81 percent that view the economy negatively.

Like all sensible people, Americans prize financial security and see it correctly as the foundation for independence and self-reliance. That is the American Way, and we recognize that it is the means to achieve the American Dream. Today’s young people believe that they are less financially secure than their predecessors, and hence being denied the Dream. Their elders agree with that assessment, Snyder writes,

A different survey that polled American adults of all ages found that 78 percent of us do not feel financially secure at this stage…

A new Intuit Credit Karma/Harris Poll study found that 78% of Americans don’t feel financially secure, even if they’ve been saving and playing by the rules.

Moreover, nearly 3 in 4 Americans (72%) shared that their current financial standing makes them feel like they will never have enough money to achieve the American dream.

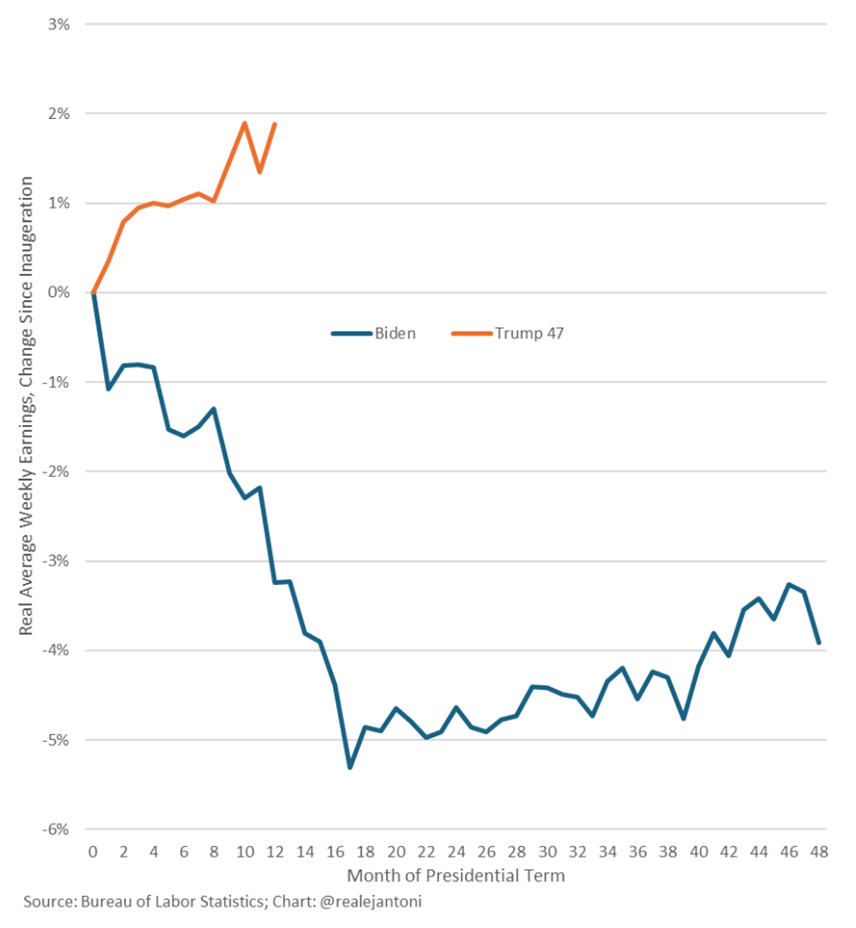

When looking at the economic statistics, however, it is difficult to justify a characterization of the economy as “bad” or “terrible” overall. The jobs market has been up and down, though generally up, and widely publicized reports of mass layoffs by big corporations are more than balanced by expansion among other companies, especially smaller ones.

On Friday, for example, The Epoch Times reported that the jobs market heated up significantly in April, at almost double the rate that economists had expected, and that employment rose much more rapidly in March than the federal government had originally stated:

April payrolls rose by 115,000, from the previous month’s upwardly revised 185,000, according to new Bureau of Labor Statistics data released on May 8.

The consensus forecast indicated a gain of 62,000 jobs.

The unemployment rate was unchanged at 4.3 percent, in line with market estimates.

For the past year, employment conditions have been typically described as “low-fire, low-hire.” New data could suggest that while the economy is witnessing a low number of layoffs, hiring could be gaining momentum.

Rising employment will ultimately drive wages even higher, as demand for workers pushes companies to compete with higher compensation and better working conditions. Additionally improving the employment picture is the fact that the new jobs are overwhelmingly in the private sector and with all the net increase in employment going to legal U.S. residents, as I wrote in Life, Liberty, Property in March of last year and other times here and elsewhere since then.

The job gains continue to arise entirely in the private sector, the Epoch Times story reports:

Federal government payrolls continued their downward trend, erasing 9,000 jobs.

“Since reaching a peak in October 2024, federal government employment is down by 348,000, or 11.5 percent,” the bureau said in the May 8 report.

“Federal employees on furlough during the partial government shutdown were counted as employed in the establishment survey because they worked or received (or will receive) pay for the pay period that included the 12th of the month.”

The employment situation is complicated and varies over time. Wages did not rise as much as economists had expected last month, the Epoch Times story notes:

Wages fell short of economists’ projections.

Average hourly earnings rose 0.2 percent monthly and edged up 3.6 percent year over year. Markets had forecast a 0.3 percent jump and a 3.8 percent reading, respectively.

The trends are positive overall, however, with after-tax real wages rising. That will greatly benefit younger workers, who are more vulnerable to changes in the job market.

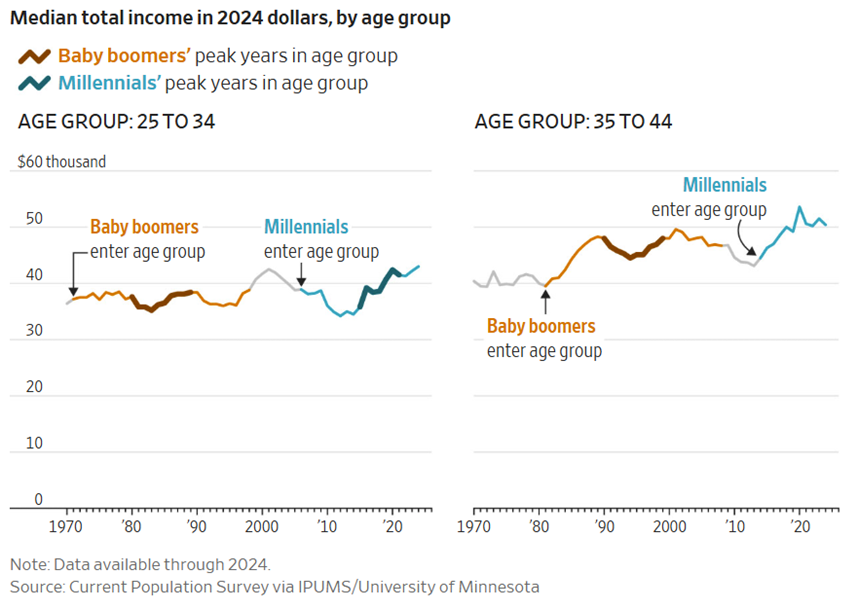

In addition, the data suggest that the claims that Millennials and Zoomers have been doing worse economically than their Baby Boomer and Gen X predecessors are inaccurate and misleading. Millennials, those born in the years 1981 through 1996, have a significantly higher real (inflation-adjusted) median income than the Boomers, born between 1946 and 1964, had at their present ages, The Wall Street Journal reported last month:

Let’s start with income. The oldest millennials are now 45, and these charts show the median individual income for them and for boomers in their early decades of adulthood, adjusted for inflation.

Millennials’ median incomes at these ages were roughly on par with Boomers’, and gains over the past decade put millennials in a better position than many recognize.

“I think that that bump up in the last 10 years still hasn’t been properly assimilated into the public conversation,” said Nathan Wilmers, a professor at MIT’s Sloan School of Management.

I’ll say it hasn’t.

Wilmers says the millennials may expect “that as our country gets richer, your income should be going up” just as fast, the MIT economist told the Journal. “Millennials rightly perceive that that has not been the case, at least in the early part of their career.”

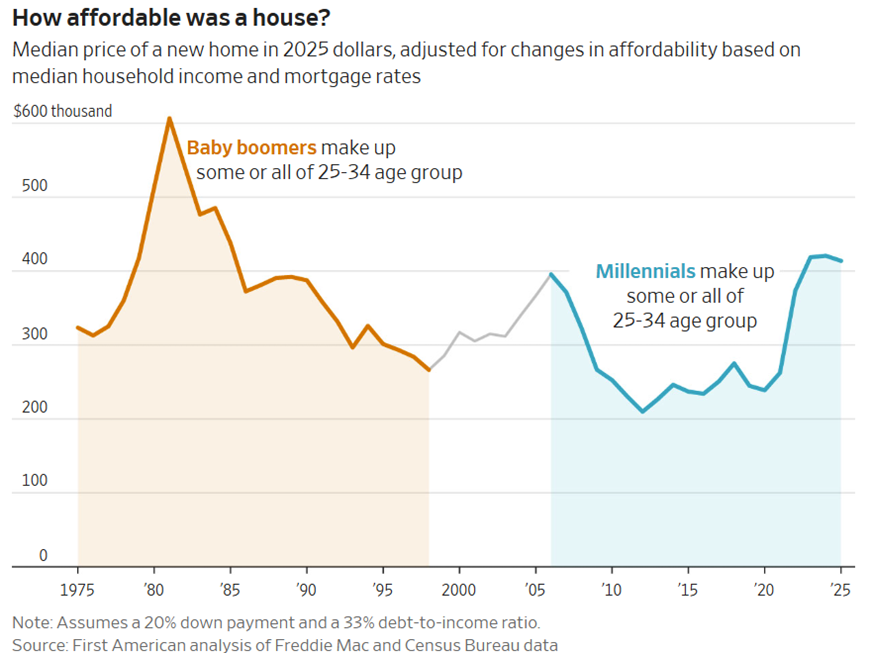

The general impression among Millennials and Zoomers appears to be that housing and other essentials are much more expensive today than when the previous generations were growing up, placing a much greater burden on today’s younger households. That is incorrect as regards housing, the Journal story notes:

One major source of tension is buying a house, an area where boomers and millennials both have a point.

Millennials looking to buy a home in the mid-2020s after a steep run-up in prices have had a tough time. But so did the boomers shopping for a house in the early 1980s, when mortgage rates peaked above 18%.

“It was indeed more expensive in today’s dollars to buy a home during that period, and pretty substantially so,” said Odeta Kushi, deputy chief economist at First American, a provider of title and settlement services.

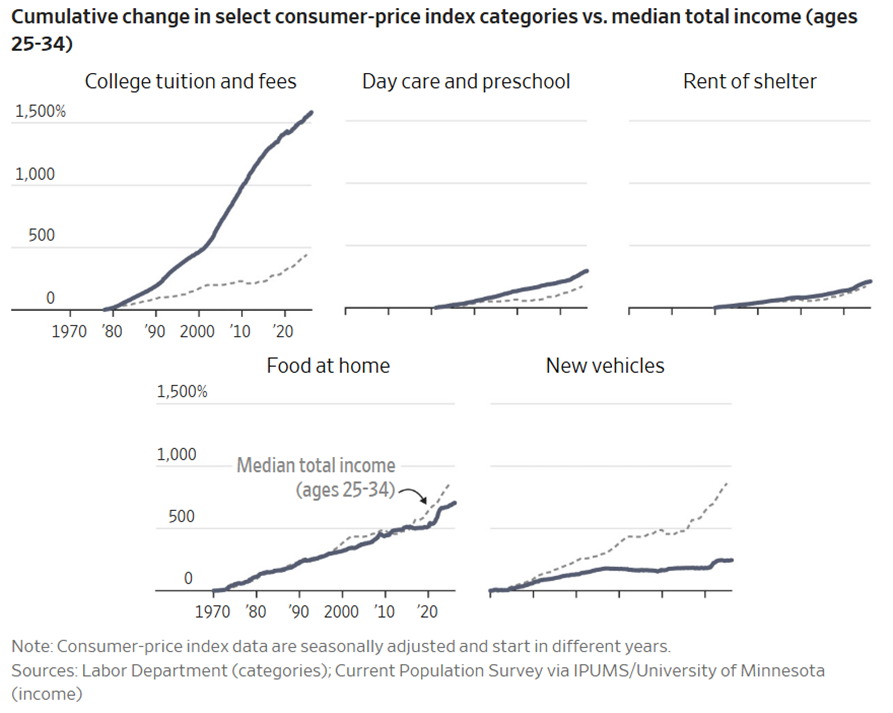

Other important items have varied in the changes in their affordability over time, the story reports:

As with housing, the costs of other individual goods and services change at different rates than overall inflation. Millennials’ incomes go further than boomers’ did on some of households’ biggest expenses, but not on others.

One item stands out in that chart: the cost of higher education has more than doubled since the Boomers attended college. Millennials have paid radically more for their college educations, and if they were anticipating a proportionate boost in income—more than two-and-a-half times what the Boomers received in median wage when they graduated from college—the Millennials’ reward has fallen far short of expectations.

In fact, younger workers with college degrees are now in greater danger of unemployment than their peers who left college after getting low-cost, two-year, associates degrees, The Wall Street Journal reports:

Among white-collar workers in tech and elsewhere, the angst is spreading. Many college-educated workers are finding it increasingly difficult to find new work after losing a job. Over the past 12 months, unemployment among college-educated workers 34 and under has converged—and now surpassed—the 4.1% rate for people with two-year associate degrees, according to an analysis of Labor Department data by the economist Gad Levanon.

The “job-security premium of a bachelor’s degree has—at least for now—disappeared,” he noted.

That is the fault of the higher education system and the federal government, not the private sector. Far from representing a market failure, the absurdly exorbitant cost and declining economic value of postsecondary education in the United States are an enormous government-installed drain on young Americans’ financial security. The federal government in particular has thrown a positively grotesque amount of money at colleges and universities to subsidize postsecondary education in recent decades. Those institutions have squandered those riches on featherbedding of a gigantic administrative caste, decreasing teaching loads, and offering luxuries designed to attract students financed by those federal government loans.

The education these institutions offer today is clearly much worse than what they gave to the Boomers and Gen X. That is why the Millennials have not received the proportionate boost in after-college income they were surely expecting: unjustifiably inflated costs have generated a vastly lower return on their investment (of borrowed money, no less).

Two generations of Americans were scammed by a sclerotic and inefficient government-dominated education system that has been corrupted at all levels under the domination of leftist careerists. Those who were subjected to this massive fraud scheme are now exceedingly angry to find themselves having been duped. Unfortunately, great numbers of them assimilated their intellectual captors’ indoctrination about the purported evils of capitalism and freedom and the imaginary beauties of socialism and serfdom, and they are directing their anger toward those who offer a better way ahead.

It is plausible, then, to see the U.S. economy today as deeply unsatisfactory when viewed from the perspective of people a few years into the working world who have been expecting a big wage advantage after paying a heavy price for a college education that the nation’s leaders promised would provide big rewards.

It should be heartening to know that today’s younger workers are receiving good wages, though it is disappointing (and rather disgusting) that they are so heavily burdened by debt for largely wasted postsecondary education. Those now heading into adulthood have taken notice and are far less enthusiastic about college. The higher-education sector is undergoing a much-needed economic reorientation that will bring lower prices and better products if the government stays out of it. (Which it seldom does, alas.)

A more realistic view of the value of postsecondary education will benefit the rising generations who arrive after the Zoomers (though they will surely suffer from other government-generated economic problems). Meanwhile, the Millennials and Zoomers will have to find a way to align their expectations with reality and not the load of hooey the government, the higher education system, and the media sold them on. They must recognize exactly who is at fault for their disappointment.

AI is everywhere; from the silly videos you see on Facebook to the articles you read online, even within hospital systems and publishers. Where is the line? Where is AI useful, and where is it more trouble than it’s worth?

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

As noted in item 1, above, the United States is suffering an affordability crisis, and especially a housing affordability crisis, that has Americans very worried about the future. Congress is considering restricting investment in housing, expanding government programs, and injecting more taxpayer money into the market. Cities are imposing rent freezes, tighter regulation, new zoning schemes, and other restrictions. Even a majority of self-identified conservatives support this approach, a poll by The Heartland Institute and Rasmussen found.

These and other such proposed government interventions will not work, however, because the problem is much bigger than alleged greed and insufficient government spending. Monetary inflation in the early 2020s and a subsequent large increase in interest rates aggravated a long-term housing affordability crunch and turned it into a housing crisis, as I have noted in past articles in this newsletter. Reducing inflation will alleviate the short-term crisis. The nation must then turn to the long-term problem: a stagnant supply of housing.

My new paper from The Heartland Institute, Housing Affordability: America’s Short-Term Crisis and Long-Term Problem, explains in easily understandable terms and illuminating charts what really caused the housing affordability crisis, why it hit Americans under the age of 40 particularly hard, what will stop that economic damage and reverse it, and how to achieve a long-term solution to America’s housing affordability problem: increasing the nation’s stagnant supply of housing.

Housing affordability has been an increasing problem in the United States as a rapidly expanding population has been forced into an increasingly insufficient housing supply since the Great Recession of 2008-2009 led to a stagnation in housing construction. A temporary but vicious bout of inflation caused by excessive government spending during and after the COVID-19 pandemic aggravated the problem into a crisis.

Focusing on those factors is the key to solving the nation’s affordability crisis: we must expand the supply of housing and ensure the reliability of the U.S. dollar. Housing Affordability: America’s Short-Term Crisis and Long-Term Problem explains why that is so, identifies the government policy actions that caused the problem, and shows how reversing them would solve it.

The paper establishes that the housing affordability problem has particularly harsh effects on those under the age of 40. Policymakers, legislators, and other government leaders are proposing many solutions, nearly all of which involve more government intervention, I note in a Heartland press release on the publication. That is how these so-called reforms usually go: they pretend to reduce the government’s power while actually expanding it.

These proposed solutions will backfire badly because they are based on a misunderstanding of the causes of the crisis. It is a product of government errors, not greedy landlords, institutional investors, and so-called market failure. The proposed interventions are also fundamentally wrong from a practical perspective: pushing investors out of the market will raise prices, not reduce them, because it will decrease investment and weaken the position of buyers, who will have to compete for an even-smaller supply of the product they want and need so badly.

A couple of my Heartland Institute colleagues provided insightful comments about the issue and my paper.

“The number one issue for nearly all Americans is affordability, particularly the high cost of housing,” said Heartland Institute Editorial Director Chris Talgo in the Heartland press release. “Although there are many factors driving the price of housing, the most sensible solution is to build more housing. However, NIMBYism, restrictive zoning practices, ridiculous environmental regulations, and many more anti-free market forces are preventing new home starts where they are most needed.

“Runaway inflation has exacerbated the housing crunch, especially for young buyers seeking starter homes,” said Talgo. “The housing market, like so many other sectors, has been undermined by big government, big spending, and big regulation. The obvious solution to the affordability crisis is less government intervention and more free market magic via the all-wise invisible hand.”

Donald Kendal, director of the Emerging Issues Center at The Heartland Institute, affirms the paper’s observation that the affordability crisis is placing an especially heavy burden on American households headed

“There is no question that America is facing a real housing affordability crisis, and younger generations are feeling the consequences most acutely,” Kendal said in the Heartland press release.

“As homeownership drifts further out of reach, more Americans are growing disillusioned with the promise of free markets and becoming more open to expansive government solutions, even socialism,” said Kendal. “But the reality is that this crisis was created by policy failures, and the path forward is not to double down on government control but rather restore a true market that allows supply to meet demand and opportunity to expand.”

America’s affordability crisis is a major symptom of the nation’s decades-long drift away from its core principles of individual liberty and market freedom, into socialism and authoritarianism. For more than a half-century, radical leftists have inculcated the nation’s children with the completely false belief that America’s history and shared culture have been overwhelmingly evil and exploitative. Young people have been taught lies about why important elements of life such as housing and marriage seem to be more difficult to obtain than they were for their parents.

The rising support for socialism in the United States is entirely a result of this enormous propaganda war. Socialist politicians, teachers, and the media tell young people that greedy people are the cause of their problems. That is a lie. The real source of our woes is power-hungry politicians and the army of dependents who give them their power. The politicians and their “nonprofit” professional-class flunkies denigrate people’s efforts to improve their lot in life, and they suppress the freedom that is necessary for such efforts, while demonizing those who achieve success through hard work and good fortune.

Free markets did not create the affordability crisis. Far from it. Today’s housing market is anything but free.

Restoring a true market is the only way to expand access to the American Dream. The way to renew the American Dream is for government to get out of the way and let Americans do things the American Way. The affordability crisis demonstrates the truth of that, as the Heartland Institute’s paper on Housing Affordability: America’s Short-Term Crisis and Long-Term Problem shows by exposing the connections between government policy and the nation’s housing problem.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org