U.S. consumer confidence declined in May in the wake of a sharp rise in inflation expectations and worries about a possible recession, The Conference Board reports:

The Conference Board Consumer Confidence Index® dipped 0.7 points to 93.1 (1985=100) in May, down from an upwardly revised 93.8 in April. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—retreated by 3.2 points to 121.2. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—rose by 1.0 points to 74.4. The survey period for this month’s preliminary results was May 1–19, encompassing the ongoing war in the Middle East that is placing upward pressure on prices globally.

The decline in consumer sentiment is justified, writes economist Robert Genetski, Ph.D., in his weekly newsletter on the economy: “comprehensive data through March for spending, incomes and inflation show the economy is slowing significantly.” Although U.S. businesses are adding jobs, inflation-adjusted personal incomes are stagnant, Genetski reports:

Personal incomes show no growth in April. for the past three- and six- month periods incomes and total wages for all workers rose by only a 3% annual rate These rates are well below our forecasts.

The income figures are very disturbing, particularly for real disposable incomes, which are down at annual rates of 4% to 6% for the past three months.

The weakness in the economy is due primarily to the personal income “inflation” measures which show inflation rates up 4% (Core) to 5% (Total) over the past six months and 5% (Core) to 6% (Total) over the past three months.

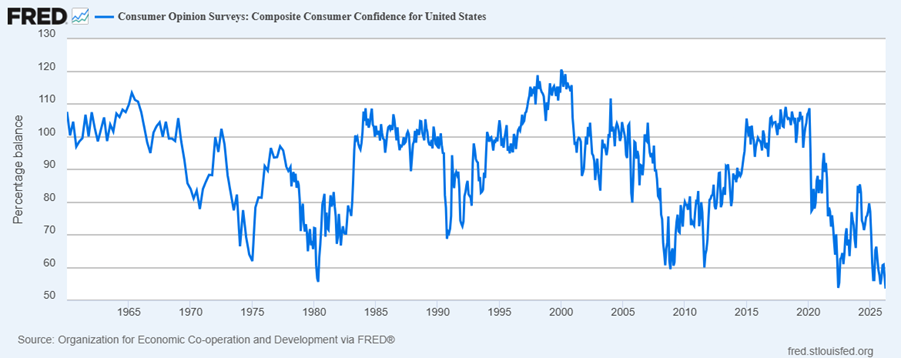

The St. Louis Federal Reserve shows consumer confidence is at a near-record low according to Organization for Economic Co-operation and Development survey data:

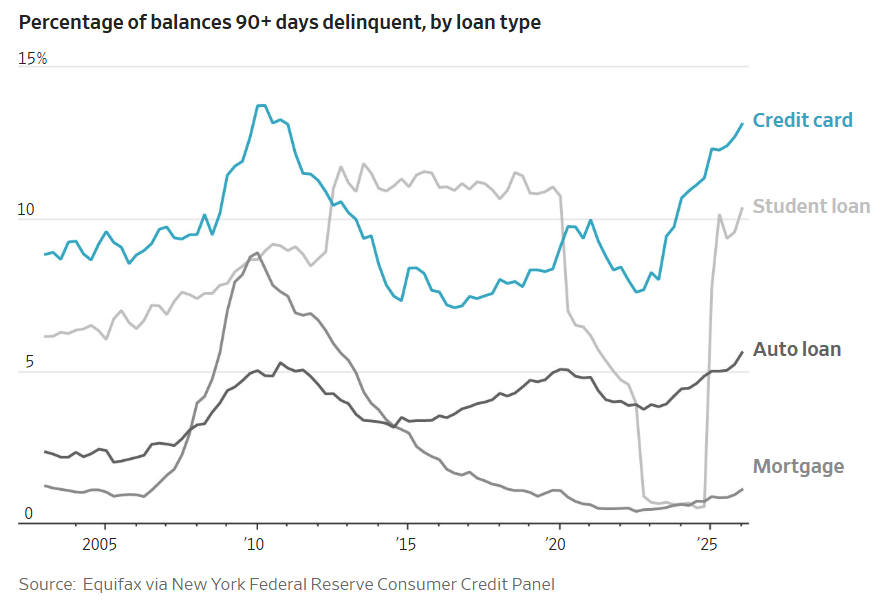

In the first quarter of this year, the percentage of credit-card balances that were at least 90 days delinquent rose to 13.12%, according to data released in May by the Federal Reserve Bank of New York. That’s the highest level in 15 years, and the most since the period following the 2008 financial crisis.

America’s total credit-card balance stood at $1.25 trillion in the first quarter, according to the New York Fed, up from $1.18 trillion in that quarter last year. That’s the highest first-quarter balance since the New York Fed began recording the measurement in 1999.

High interest rates are giving consumers fits. “Average interest rates on cards rose to 21% in February, from 14.6% in February 2022, according to a survey of credit-card issuing banks by the Federal Reserve,” the Journal reports.

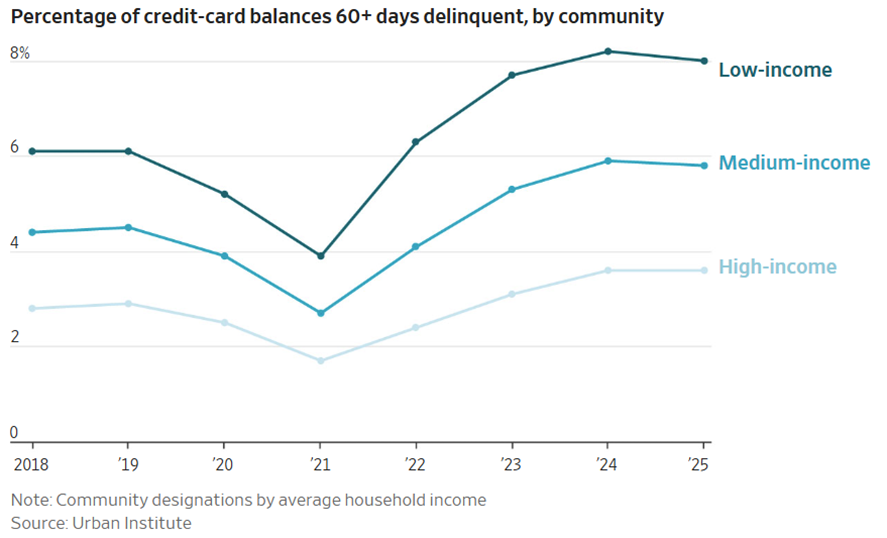

People at all levels of income are falling behind on their payments, the story reports (though I doubt that this applies to those with the highest incomes):

Last year, 5.6% of credit-card holders were 60 days or more behind on their payments, surpassing prepandemic levels, according to data compiled by Breno Braga, an economist with the Urban Institute, a left-of-center research group. Over the past two years, his analysis showed, the rate rose to its highest level since 2018 for residents of lower, middle and upper-income communities alike.

Low-income people are falling farthest behind, as usual, the Journal notes:

The jump in interest rates is making it especially hard for those on low economic rungs to dig out of debt. Cardholders in low-income communities—ZIP Codes with an average household income less than $89,500—had 60-day delinquencies of 8%, the highest rate of any income level, according to Braga’s analysis.

The sharp increases in inflation and interest rates in May in response to the closing of the Strait of Hormuz and consequent jump in oil prices account for Americans’ increasing financial struggles and pessimism about the economy.

An agreement to end the conflict in Iran and get oil tankers moving freely out of the Persian Gulf would relieve those acute current pressures. The United States and Iran are reportedly heading toward a 60-day extension of the cease-fire, with Iran expected to make the requested major concessions, as I write on Friday afternoon. That will go a long way to restore economic confidence within the United States.

The long-term problem of government suppression of the U.S. economy remains, however. American producers, consumers, and investors need a better environment in which to work: far less government spending, lower interest rates (which spending cuts would enable), and removal of the miasma of unnecessary federal regulations that are encoded in statute and require congressional action.

Leftists are being irresponsible with other people’s money: in New York City, Mayor Mamdani is openly bragging about his plans to take properties from landlords who own them, and transfer ownership to nebulous “responsible stewards.” This is totally unsurprising coming from the socialist mayor, but we will discuss WHY socialists and communists hate private property, and the government schemes that link rent control to redistribution.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Surprising Crime-Reduction Success Story in Baltimore

After many years as a real-life horror movie of criminal takeover and urban decline, Baltimore, Maryland, has become a surprising success story in rapidly and radically reducing violent crime.

Two significant policy changes seem to have driven this highly beneficial social change, Manhattan Institute fellow Charles Fain Lehman reports at The Free Press. In just six years, Baltimore transformed from a murder factory into a much safer place:

The 2015 riots, in response to the death of 25-year-old Freddie Gray in police custody, inaugurated a retreat in Baltimore policing and a multiyear surge in street violence. In 2020, amid a national increase in killings, the Charm City saw homicide rates about eight times higher than the national average.

Then, in late 2022, Baltimore’s fortunes turned. Starting sometime late in the calendar year, murder rates started plummeting. The city reported 333 murders that year. Last year, after three years of steady decline, there were just 133 murders in the whole city—a more than 60 percent drop. That’s the fewest murders Baltimore has seen since 1965.

Although urban leaders commonly cite vague, ill-defined social conditions as causing crime, police and prosecution appear to be the deciding factors, Lehman notes:

The bigger lesson is that intelligently targeting the most violent offenders, both through deterrence and incapacitation, can yield large, durable reductions in murder. Baltimore’s success shows that its homicide problem was, in reality, just the result of its past leaders’ failure to take violence seriously enough.

Young males are far more prone to commit violent acts than other people are, and trouble often escalates when they meet, Lehman writes:

Statistically speaking, almost no one reading this article will be murdered. Out of the 3,072,666 deaths in the United States in 2024, 20,162 were homicides, Centers for Disease Control and Prevention data show. If you live outside of one of a handful of murder hot spots, your risk falls even lower. Even within these areas, you need the right ingredients for a high homicide rate: groups of young men with guns, a tendency to get into personal “beefs,” and little social oversight.

When you mix that recipe together, though, things can get insanely dangerous. In parts of some American cities, research has shown, young men have a higher rate of homicide death than did U.S. soldiers serving in Iraq and Afghanistan. This hyperconcentration of violence has shown up in Washington, D.C.; Chicago; Oakland, California; and elsewhere. The networked nature of the violence is important. Killers and victims are often tied up in the same social networks, meaning that beef between group members can continually escalate in a cycle of retaliation.

Baltimore follows this pattern.

The numbers are so staggering as to be almost preposterous, yet they are true. As I have reported before (specifically mentioning Baltimore), hitting crime hotspots with a strong police presence is essential. The data fully support that conclusion. Lehman writes,

In Baltimore’s Western District, 72 percent of murders between 2015 and 2021 were attributable to a small number of men, mostly organized into gangs. The same analysis estimated that the area’s gang members accounted for just 2 percent of the district’s population but as much as 75 percent of its shootings and homicides.

The threat of arrest and prosecution has a strong, positive effect in reducing crime, Lehman reports:

Braga and Harvard Kennedy School colleagues David Kennedy and Anne Piehl designed a strategy variously called Group Violence Intervention, focused deterrence, or “Operation Ceasefire.”

They gathered up the frequent offenders, well-known to police, and had officers issue a clear message: Violence would no longer be tolerated. Community organizations offered help—with jobs, records, and so on. But the overwhelming message was that if these offenders offend again, the law will come down on them like a ton of bricks.

The strategy worked. Youth homicides fell 63 percent, while the number of “shots fired” incidents fell 32 percent.

It is important to recognize that this approach is not just talk. It includes a serious threat of arrest and imprisonment. Lehman writes,

The approach involves a detailed investigation of every shooting that happens in the city. Every week, the Baltimore Police Department and its partners review the week’s incidents. They make plans to arrest anyone who has committed a crime or violated parole. Occasionally, the program leads to tips that end in an arrest.

But mostly the focus is on deterring the cycle of escalation. GVRS has yielded about 600 arrests in its five years of operation. For every shooting, GVRS prescribes reaching out to known associates of the victim. A second weekly meeting brings together law enforcement officials with service organizations and “community moral voices”—respected neighborhood figures who can put pressure on a would-be shooter to stand down.

Incarceration is not a plausible threat or deterrent, however, if prosecutors decline to bring cases to trial. From 2016 through 2022, Baltimore’s top prosecutor did exactly that, refusing to prosecute multiple types of crimes and perversely pursuing action against the police. Lehman reports,

Something else has changed in Baltimore: its top prosecutor.

In 2015, Baltimore elected Marilyn Mosby as its state’s attorney. She was the nation’s youngest big-city prosecutor, part of the wave of “progressive prosecutors” that swept into office. Backed by left-leaning activists, these prosecutors sought to use their discretion to unilaterally decriminalize a host of petty offenses in the name of ending mass incarceration.

Mosby almost immediately got a chance to prove her bona fides. Shortly after her election, Freddie Gray died after a “rough ride” in a police van following a misdemeanor arrest for possession of a knife. In a predominantly black city already primed by the Ferguson, Missouri, protest movement, Gray’s death lit the powder keg. The ensuing protests and riots drove a spike in violence in the city that arguably did not abate until 2023. Mosby stepped in, not to put an end to the disorder but to lead a failed attempt to prosecute the officers involved in Gray’s death.

In 2021, her office stopped prosecuting drug possession, prostitution, trespassing, and “other low-level offenses” entirely. Unsurprisingly, the ensuing surge in crime made her unpopular with voters. So, too, did her indictment for perjury and making false statements on mortgage applications. In 2022, Mosby lost reelection. (She spent a year in home confinement after being convicted of mortgage fraud and perjury, though the fraud conviction was overturned.)

With Mosby out of the way, the state’s attorney’s office resumed prosecution of criminals and stopped harassing the police, Lehman writes:

Mosby’s replacement was Ivan Bates, a former defense attorney who had represented one of Gray’s alleged killers. On the campaign trail, Bates took Mosby to task for her corruption and the city’s crime problems, promising to focus on gun violence and on building bridges between the community and law enforcement. Since taking office, Bates has made prosecuting violent offenders his top priority. …

Bates said that his office has identified about 6,000 frequent, violent offenders and put between 3,000 and 3,500 of them in prison. The cooperation of federal law enforcement has helped take a number of these offenders off the streets.

Lehman argues that success in reduction of violent crime requires both approaches: concentrating police efforts on the most likely offenders and reliably prosecuting those who commit the crimes:

In a sense, it is impossible to know which made the difference. But trying to credit one or the other obscures how crucially they work together. GVRS keeps violence from escalating, reducing opportunities for offending in the first place. At the same time, locking up thousands of violent repeat offenders will incapacitatethem. But GVRS’s deterrence can’t work if the threat of incarceration isn’t credible. A good prosecutor is the linchpin to a successful deterrent strategy.

Both those policies are obviously necessary, as common sense and decades’ worth of crime statistics tell us. It is dismaying, disappointing, and tragic that city leaders all across the United States regularly deny the need for these simple and effective law enforcement actions. “Baltimore shows other cities struggling with violence that murder is a problem that we know how to solve: Lock up offenders and deter further escalation,” Lehman writes. “The only question is: Do more leaders have the will to do it?

Lehman does not discuss why this sensible approach requires “will,” meaning courage.

I’ll explain it, then. Much of the policy discussion on crime prevention is tainted by concerns about a racial disparity in crime rates, as Lehman’s article indicates without saying it outright, a factor that is obvious to anyone who pays even the slightest attention to the debates. The great majority of violent crimes are not interracial, however, which makes laxity in crime prevention vastly more harmful to any race that has a high crime rate.

The way to provide equal crime-protection to people of all races is to base pursuit and prosecution solely on each individual’s actions. That is the only fair and equitable way to deal with crime and criminals, and it reduces crime and saves lives.

It is shameful that so many politicians and advocacy organizations around the country would rather people lose their lives than lose their illusions.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

International Extortionists Go After American Farmers

Big corporations are imposing an expensive, economically destructive climate-change agenda on American farmers, Heartland Institute Senior Manager for Government Relations Samantha Fillmore writes at The American Spectator:

It starts with a letter in the mail.

A dairy farmer opens it to find new requirements from their milk processing plant. Herd data, energy usage, emissions figures. The letter calls it voluntary but if you don’t comply, the plant can’t take your milk. And if the plant can’t take your milk, you’re out of business.

That’s Pathways to Dairy Net Zero in practice.

Pathways to Dairy Net Zero (P2DNZ) is presented as a voluntary, science-based initiative to reduce greenhouse gas emissions from dairy producers. In practice, however, it functions as yet another sector-specific implementation of global ESG and net-zero governance.

Encouraged by international nongovernmental organizations, powerful multinational corporations are forcing this agenda on milk processors, under threat of debanking, declining land values, inability to buy insurance, and other ways of putting them out of business. The dairy farms that supply the milk to the processors must either comply with the requirements or find other ways to sell their products, which is infeasible given the web of federal and state regulations on agricultural products.

The P2DNZ requirements threaten farmers with bankruptcy, Fillmore writes:

In the case of P2DNZ, this governance model is applied to large-scale milk producers. The result is the downward transfer of climate-compliance costs and onerous ESG restrictions on farmers[, e]specially mid-sized and small farms, while offering no plausible pathway to detectable global emissions reductions. In short, this is the latest attack on American farmers from globalist board rooms seeking to control what you consume.

P2DNZ may be presented as a voluntary, science-based initiative but in reality, it’s the same ESG playbook we’ve seen used to squeeze entire industries into net-zero compliance without a single vote being cast. The pressure doesn’t come from government. It comes from the giant food corporations at the top of the supply chain. It comes from the boardrooms of companies like Nestlé and Danone and filters down through processors until it lands on the farmer who has no real choice but to comply.

What begins as “guidance” quickly becomes obligation.

The scheme does nothing to slow or eliminate climate change. Instead, the system transfers power and wealth away from American farmers, processors, and, most importantly, consumers, and gives it to multinational and/or foreign power brokers. Fillmore writes,

Even under the most aggressive assumptions, eliminating all emissions from U.S. dairy production would have no detectable impact on global climate trends. That’s not a political statement; it’s a matter of scale. Yet the economic consequences are anything but theoretical. Farmers face rising compliance costs. Consumers face higher prices at the grocery store. And the industry itself faces increasing consolidation, as smaller producers struggle to keep up with mandates they had zero role in shaping.

This is the uncomfortable truth at the heart of P2DNZ: it is less about environmental outcomes and more about control. It’s about shifting decision-making power away from independent producers and toward a network of globalist financial and corporate actors.

The P2DNZ is nothing less than a globalist extortion scheme. It is designed to impose foreign control on a critical sector of the U.S. economy and threaten Americans and others around the world with hunger and possible starvation should they try to resist this takeover. Fillmore writes,

The attacks on American agriculture have taken on many forms. From discriminating against the use of diesel- and gasoline-powered farming equipment in the lending market, to corporate shareholder resolutions calling on food companies to “reduce greenhouse gas emissions” by cutting beef production, to utter demands to adopt plant-based alternatives to actual meat, and even outright litigation designed to bankrupt American businesses and farmers. Regardless of the tactic, they share a common objective. To create a world in which every single human is under the thumb of a global set of rules that would ensure more pain and misery than anyone should entertain.

Fortunately, the Trump administration is aware of this activity and is working to protect “small- and mid-sized American farms and dairy producers,” Fillmore writes. In fact, Agriculture Secretary Brooke Rollins cited Heartland’s work on the issue, in a series of X posts. “Dairy farmers are vital in rural America, but now face radical ESG mandates disguised as ‘sustainability.’ As (@Heartland Impact) notes, Pathways to Dairy Net Zero will burden small farms with costly compliance,” Rollins wrote.

As Fillmore’s article and other writings note, ESG and net zero are not about protecting the global climate. They are about controlling the global economy.

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org